Various events are set to impact the markets this week, most notably the rate decisions of major central banks including the Reserve Bank of Australia and the Bank of Canada. Traders are advised to exercise caution and stay informed about the latest developments to ensure a successful week of trading.

Here are the upcoming market highlights for the week:

Reserve Bank of Australia Rate Statement (5 December 2023)

The Reserve Bank of Australia raised its cash rate by 25 bps to 4.35% in November after maintaining it at 4.1% following its previous four meetings.

Analysts predict that the central bank will keep its cash rate at 4.35% after its upcoming meeting on 5 December.

US ISM Services PMI (5 December 2023)

The Institute of Supply Management (ISM) Non-Manufacturing PMI—also known as the US ISM Services PMI—fell to 51.8 in October, the lowest in five months.

Updated figures will be released on 5 December, with analysts expecting an updated PMI of 52.

Australia Quarterly Gross Domestic Product (6 December 2023)

The Australian economy expanded by 0.4% in Q2 2023.

Analysts predict that the data for Q3, scheduled to be released on 6 December, will indicate slower expansion at 0.3%.

Bank of Canada Rate Statement (6 December 2023)

The Bank of Canada kept the target for its overnight rate at 5% following its October 2023 meeting.

Its next rate statement is scheduled to be released on 6 December, with analysts anticipating that the rate will remain at 5%.

US Jobs Report (8 December 2023)

The US economy added 150,000 jobs in October, a decrease from the 297,000 jobs added in September. Meanwhile, the unemployment rate increased to 3.9% in the same period, slightly exceeding the previous month’s figure of 3.8%.

Updated figures will be released on 8 December, with analysts forecasting the addition of 180,000 more jobs and an unemployment rate of 3.9%.

University of Michigan Consumer Sentiment Index (8 December 2023)

The University of Michigan Consumer Sentiment Index for the US was revised to 61.3 in November from a preliminary figure of 60.4, but it still remained at its lowest level since May.

Updated figures will be released on 8 December, with analysts expecting the index to hit 61.8.

As part of our commitment to provide the most reliable service to our clients, there will be server maintenance this weekend.

Maintenance Hours :

2nd of December 2023 (Saturday) 00:00-05:00 (GMT+2)

Please note that the following aspects might be affected during the maintenance:

1. The price quote and trading management will be temporarily disabled during the maintenance. You will not be able to open new positions, close open positions, or make any adjustments to the trades.

2. There might be a gap between the original price and the price after maintenance. The gaps between Pending Orders, Stop Loss and Take Profit will be filled at the market price once the maintenance is completed. If you don’t want to hold any open positions during the maintenance, it is suggested to close the position in advance.

3. Please refer to MT4/MT5 for the latest update on the completion and market opening time. Our services will be back online once the maintenance is completed.

Thank you for your patience and understanding about this important initiative.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com

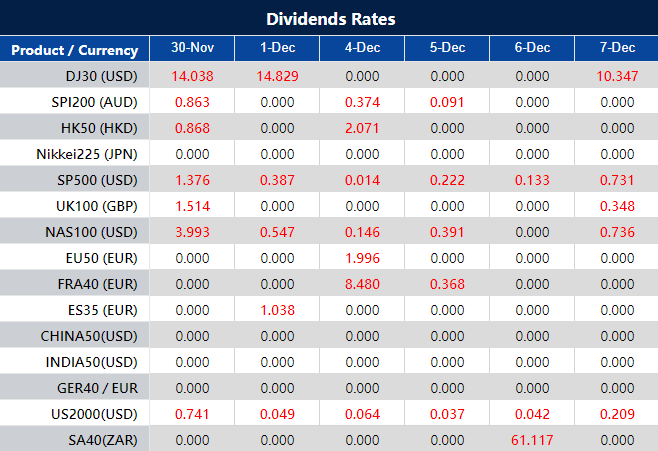

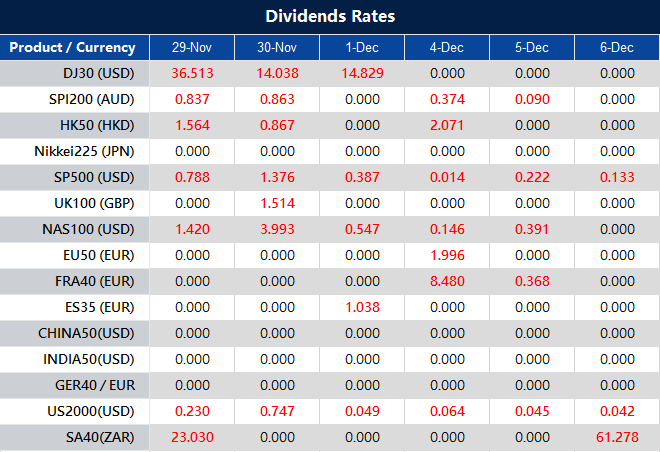

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

November witnessed robust stock market rallies with the Dow Jones surging to a new yearly high, marking an 8.9% gain while the S&P 500 and Nasdaq also experienced significant growth. Cooling inflation figures hinted at a potential shift in the Federal Reserve’s policy, driving investor optimism. Tech stocks like Nvidia, Tesla, Alphabet, and Meta dominated gains, albeit facing slight declines towards month-end. Simultaneously, the dollar rebounded against the euro due to position adjustments and surprising euro zone inflation data, influencing expectations of rate adjustments by both the Fed and ECB. Amidst various currency movements, the anticipation of key economic reports and Fed Chair Powell’s remarks played pivotal roles in market dynamics.

Stock Market Updates

In November, the stock market witnessed a strong rally, with the Dow Jones Industrial Average surging to a new yearly high and closing at 35,950.89, marking an impressive 8.9% gain for the month. The S&P 500 also experienced substantial growth, climbing 8.9%, while the Nasdaq Composite, though slightly lower by 0.2%, still managed a solid 10.7% advance. This surge was primarily fueled by cooling inflation figures, indicating a potential shift in the Federal Reserve’s monetary policy. Despite the broader market’s gains, some profit-taking in Big Tech stocks caused a minor dip in the Nasdaq on Thursday. However, positive earnings reports from Salesforce, driven by its robust cloud data business and AI product, boosted the Dow alongside leading healthcare companies like UnitedHealth Group, Johnson & Johnson, Merck, and Amgen.

The market sentiment was buoyed by indications that inflation might be stabilizing, as the personal consumption expenditures price index rose by 3.5% year-over-year, slightly lower than the previous month’s 3.7% increase. This trend led investors to speculate that the Federal Reserve could potentially halt rate hikes and even consider rate cuts by 2024. Additionally, the 10-year Treasury yield, after reaching above 5% the previous month, dipped to 4.34% in response to the cooling inflation figures, elevating confidence in equities. Technology stocks had dominated November’s gains, with Nvidia, Tesla, Alphabet, and Meta showcasing substantial increases throughout the month, though some investors chose to realize profits as November drew to a close, resulting in slight declines for these tech giants on Thursday.

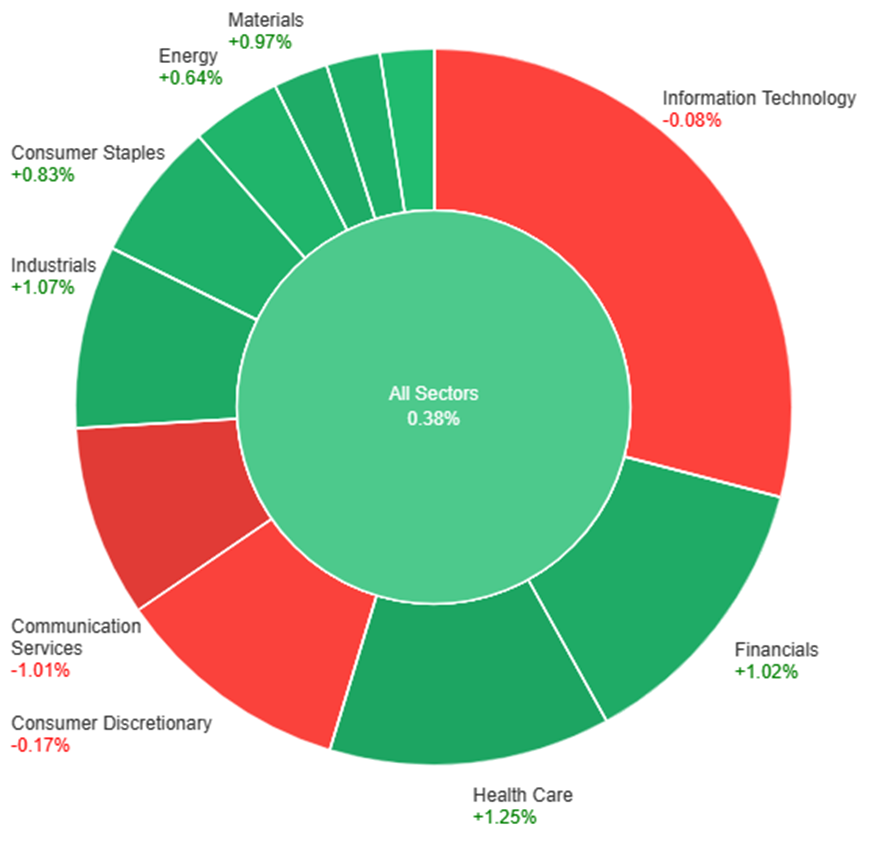

On Thursday, across the various sectors, the market showed a general upward trend with an overall gain of 0.38%. Notably, Health Care exhibited the most substantial growth, rising by 1.25%, followed closely by Industrials and Financials, which saw increases of 1.07% and 1.02%, respectively. Materials and Consumer Staples also experienced notable gains at 0.97% and 0.83%. Real Estate and Energy sectors showed moderate growth at 0.83% and 0.64%, respectively. Conversely, Information Technology experienced a slight dip at -0.08%, while Consumer Discretionary and Communication Services showed more significant declines of -0.17% and -1.01%, respectively.

Currency Market Updates

In the latest currency market updates, the dollar rebounded at month-end, benefitting from position adjustments and a surprising drop in eurozone inflation compared to forecasts. Despite soft U.S. economic data, including personal income, spending, and core PCE figures, EUR/USD declined by 0.7%. The market’s anticipation of Federal Reserve Chair Jerome Powell’s forthcoming comments and the impending jobs report next week contributed to the dynamics. The dollar index experienced a 0.7% decline while finding support near the 61.8% retracement of the July-October advancement, yet the rebound was capped by the 200-day moving average at 102.57.

EUR/USD’s downward movement overlooked the subdued U.S. economic data, alongside expectations in the futures market of potential earlier and more substantial European Central Bank (ECB) rate cuts compared to the Fed’s projections for next year. The bearish trend in 2-year bund-Treasury yield spreads, diverging from rising EUR/USD prices since mid-November, added to the downward pressure. The currency pair may find support around the previous week’s low of 1.08525 and the November 17 swing low, as investors await further U.S. data.

Additionally, other major currencies reacted to the dollar’s resurgence: Sterling fell by 0.58%, while USD/JPY rose by 0.65% in its month-end rebound. These movements were influenced by technical levels, such as Fibonacci retracements, and the interplay between key moving averages. The broader scenario was influenced by the anticipation of yield spread dynamics between the Treasury and JGB (Japanese Government Bonds) and the Fed’s gradual shift towards easing, contributing to the possibility of substantial losses into 2024. Economic events such as the U.S. ISM manufacturing data for November, Powell’s policy comments, ISM non-manufacturing, JOLTS, and Friday’s non-farm payrolls report were anticipated as market movers in the coming days.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Faces Consolidation Amid Divergent Economic Data and Central Bank Speculations

The EUR/USD pair witnessed a notable pullback, hitting a low of 1.0883 after a recent surge past 1.1000. With the Eurozone CPI registering a slower annual increase in November, lingering below the ECB’s target, speculation looms regarding potential rate cuts. This news, coupled with the Euro’s lag against the Swiss Franc, hints at a short-term downside risk for the Euro. Meanwhile, the US Dollar, bolstered by recovering Treasury yields despite mixed US data, showcased resilience. As the market eyes the upcoming US ISM Manufacturing PMI release and ECB monetary policy, the pair remains poised for consolidation amidst divergent economic trends and central bank anticipations.

On Thursday, the EUR/USD experienced a downward movement, creating a push to the lower band of the Bollinger Bands. Currently, the price moving slightly above the lower band, suggesting a potential upward movement, potentially reaching the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 40, signaling a neutral with a slight bearish outlook for this currency pair.

Resistance: 1.0945, 1.1041

Support: 1.0842, 1.0760

XAU/USD (4 Hours)

XAU/USD Edges Down as Inflation Data Favors Rate-Cut Speculations

Gold prices slightly declined on Thursday as investors pivoted away from safe-haven assets in response to the release of US inflation data. The Core PCE Price Index rose by 0.2% MoM and 3.5% YoY in October, aligning with expectations but falling below September’s figures. This news was embraced by financial markets as an indication of the Fed’s likely shift toward a rate-cut monetary policy. Simultaneously, major economies like the Eurozone witnessed diminishing price pressures, evidenced by a decline in HICP figures. This trend bolstered hopes that central banks may forego additional rate hikes, averting a severe economic downturn. The flight from safety also impacted government bonds, propelling yields upwards, with the 10-year Treasury note at 4.32% and the 2-year note at 4.69%, although notably lower than previous peaks recorded in October.

On Thursday, XAU/USD moves in a period of consolidation, currently oscillating between the middle and upper bands within the Bollinger Bands. This current movement suggests a potential upward trend, potentially reaching the upper band once again. The Relative Strength Index (RSI) stands at a level below 63, indicating that the bullish sentiment for this pair remains robust.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Written on November 30, 2023 at 6:54 am, by anakin

As November draws to a close, U.S. stock futures indicate a favorable end to the month for major indexes, propelled by surges in Salesforce and Snowflake following stellar earnings. Despite marginal movements in the Dow and S&P 500, both remain near their year-to-date highs, while the Nasdaq holds close to its 2023 peak. November promises to break the three-month losing streak, with the S&P 500 up 8.5% and Nasdaq near 11%, marking their strongest performance since July 2022. Positive market sentiments contrast declines in Asia-Pacific markets, with the focus shifting to potential Federal Reserve rate cuts in 2024. In the currency market, the dollar rebounded on speculations of faster rate cuts, impacting forex pairs and stirring market uncertainties amidst varying economic indicators and central bank remarks.

Stock Market Updates

In November’s final stretch, U.S. stock futures edged up, signaling a positive closure for the month across the major indexes. Wednesday’s after-hours trading saw Salesforce and Snowflake soaring due to better-than-expected earnings, with Salesforce marking an 8% surge and Snowflake climbing over 7%. Despite a marginal day for the Dow and S&P 500, both indexes hover just around 0.5% and 0.8%, respectively, from their year-to-date closing highs. Similarly, the Nasdaq Composite, though slipping 0.16% during the day, remains close to its 2023 closing high by about 0.7%.

November appears poised to end the three-month losing streak for the major indexes, with the S&P 500 marking an 8.5% gain and the Nasdaq nearly reaching an 11% increase. These figures represent their most robust monthly performance since July 2022. The Dow, up by 7.2% in November, is also on track for its best month since October 2022. Amidst higher interest rates, strategist Jay Woods remains optimistic about stocks holding onto their gains, citing positive price action and supportive economic data for the Fed’s stance on rates.

European stocks closed higher, reclaiming positive momentum as markets assessed Federal Reserve board members’ statements. The Stoxx 600 index closed 0.43% higher, with Germany’s DAX index maintaining gains above 1% following a report indicating a slowdown in German inflation for November, surpassing earlier forecasts. Meanwhile, Federal Reserve Governor Christopher Waller expressed growing confidence in the Fed’s policies to rein in inflation, hinting at potential rate reductions if inflation continues to ease in the next few months. However, despite a slight retreat in Wall Street’s earlier gains, the major U.S. indexes remained on course for significant gains in November, contrasting the overnight declines in Asia-Pacific markets, primarily led by losses in Hong Kong.

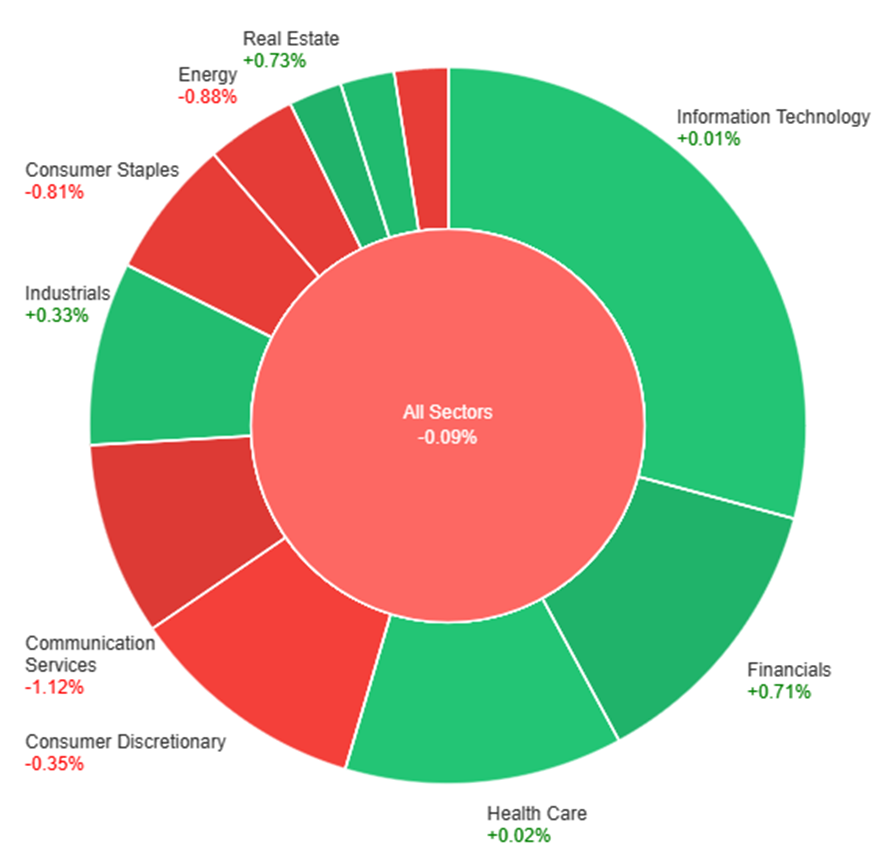

On Wednesday, the overall market experienced a slight decline of 0.09%. However, several sectors showed positive movements, with Real Estate leading the gains at +0.73%, followed closely by Financials at +0.71% and Materials at +0.38%. Industrials and Health Care also saw modest increases of +0.33% and +0.02%, respectively. Conversely, there were notable decreases in certain sectors, with Communication Services taking the biggest hit at -1.12%, followed by Energy at -0.88%, and Consumer Staples at -0.81%. Utilities and Consumer Discretionary also faced declines of -0.79% and -0.35%, respectively. Overall, while some sectors thrived, others encountered notable downturns during the trading day.

Currency Market Updates

In the currency market, the dollar index experienced a rebound of 0.14% after reaching oversold levels, largely influenced by speculation surrounding faster Federal Reserve rate cuts in 2024. This sentiment emerged following comments from Fed’s Waller, leading to expectations of a rate cut as early as May, with futures indicating a potential 114 basis points of cuts by 2024. Concurrently, the Euro saw a decline against the dollar, notably influenced by below-forecast German CPI, fostering a 42% probability of an ECB rate cut in March with an estimated 110 basis points of cuts by the end of 2024. The EUR/USD pair retraced to 1.0960, marking a critical level in its July-October slide.

While the dollar’s trajectory was influenced by expectations around Fed rate cuts, the market remained attentive to upcoming data releases and central bank remarks. The discrepancy among Fed speakers regarding progress in the inflation fight juxtaposed against economic indicators like Q3 GDP revisions, softer Q4 data, and core PCE adjustments to 2.3% contributed to the uncertainty. The movement of key pairs like USD/JPY, impacted by tumbling Treasury yields and contrasting JGB yields, indicated potential challenges for hefty speculative dollar longs. Amidst these fluctuations, sterling rose as it retraced a significant portion of its previous decline, echoing the broader market sentiment awaiting U.S. data releases and Fed Chair Jerome Powell’s commentary. Additionally, the Aussie and Chinese yuan pairs experienced declines and rebounds, respectively, influenced by below-forecast inflation and fluctuations in Fibonacci retracement levels indicative of market sentiment shifts.

The EUR/USD surged to a three-month high at 1.1016 but retreated below 1.1000 despite burgeoning risk appetite. Europe witnessed a slowdown in inflation, notably in Germany and Spain, raising concerns about potential ECB rate cuts. Yet, this might not prompt immediate dovish action, as analysts anticipate a rebound in inflation over the next months. Meanwhile, the US economy revealed robust growth of 5.2% in Q3, lifting the US Dollar on confidence in its performance. However, recent indications of a slowdown before November 18 from the Beige Book compounded with upcoming critical US data—Core PCE Price Index and Jobless Claims—could exert further pressure on the Greenback if they reflect softening inflation and labor market conditions. Bond yields fell on both sides, especially in Germany, adding to the volatility gripping the EUR/USD pair.

On Wednesday, the EUR/USD experienced a downward movement, settling around the middle range of the Bollinger Bands. Presently, the price exhibits a marginal increase above this midpoint, suggesting a potential upward trajectory, potentially reaching the upper band. Notably, the Relative Strength Index (RSI) maintains its position at 55, signaling a neutral outlook for this currency pair.

Resistance: 1.1041, 1.1087

Support: 1.0968, 1.0930

XAU/USD (4 Hours)

XAU/USD Dips Amid Dollar’s Recovery and Fed’s Inflation Sentiments

Spot Gold slid to $2,040 an ounce, pulled down by a resurgent US Dollar amidst profit-taking before pivotal data releases. Despite the Dollar’s bounce, its weakness persists on hopeful sentiments that the Federal Reserve might halt tightening measures. Conflicting views within the Fed add to the uncertainty: while Atlanta Fed President Bostic signals confidence in declining inflation, Richmond Fed President Barkin remains cautious, keeping the possibility of rate hikes alive. With US bond yields retreating to multi-week lows and market focus shifting to the upcoming inflation data, Gold’s trajectory hinges on signs of easing price pressures, poised to either bolster optimism or dampen USD demand.

On Wednesday, XAU/USD underwent a period of consolidation, presently oscillating between the middle and upper bands within the Bollinger Bands. This current movement suggests a potential upward trend, potentially reaching the upper band once again. The Relative Strength Index (RSI) stands at a level below 69, indicating that the bullish sentiment for this pair remains robust.

Resistance: $2,052, $2,079

Support: $2,038, $2,012

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

ALL

OPEC-JMMC Meetings

All Day

CAD

GDP m/m

21:30

0.0%

USD

Core PCE Price Index m/m

21:30

0.2%

USD

Unemployment Claims

21:30

219K

Written on November 30, 2023 at 2:35 am, by anakin

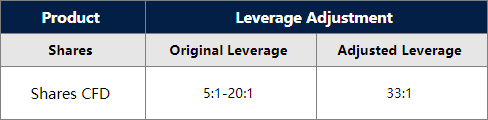

To provide a favorable trading environment to our clients, VT Markets will modify the trading setting of all share CFDs on Dec 4, 2023:

1. All Shares leverage is adjusted back to 33:1, and the leverage adjustment during opening and closing are cancelled.

2. 20 Pre-market US shares on MT5: Leverage will be 5:1 during 22:45-23:00 and 14:00-16:30 ; and remain 33:1 during the rest of the trading time.

3. The above data is for reference only, please refer to the MT4 and MT5 software for specific data.

Friendly reminders:

1. All specifications for Shares CFD stay the same except leverage during the mentioned period.

2. The margin requirement of the trade may be affected by this adjustment. Please make sure the funds in your account are sufficient to hold the position before this adjustment.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Written on November 30, 2023 at 2:27 am, by anakin

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Written on November 29, 2023 at 9:06 am, by anakin

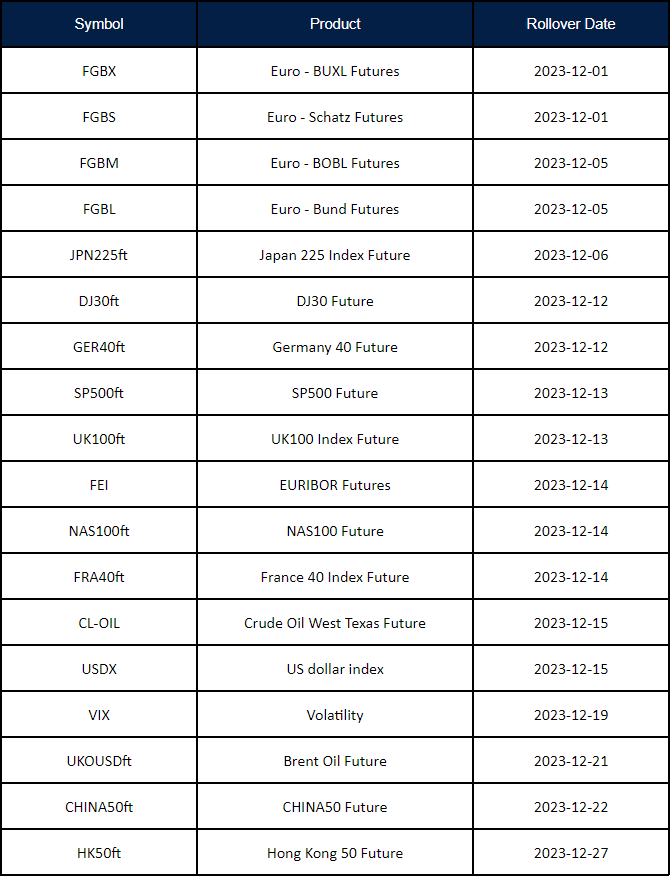

New contracts will automatically be rolled over as follows:

Please note:

• The rollover will be automatic, and any existing open positions will remain open.

• Positions that are open on the expiration date will be adjusted via a rollover charge or credit to reflect the price difference between the expiring and new contracts.

• To avoid CFD rollovers, clients can choose to close any open CFD positions prior to the expiration date.

• Please ensure that all take-profit and stop-loss settings are adjusted before the rollover occurs.

• All internal transfers for accounts under the same name will be prohibited during the first and last 30 minutes of the trading hours on the rollover dates.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Written on November 29, 2023 at 9:02 am, by anakin