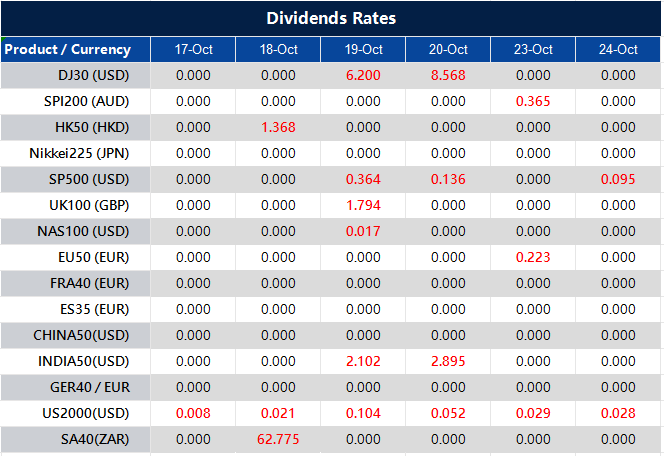

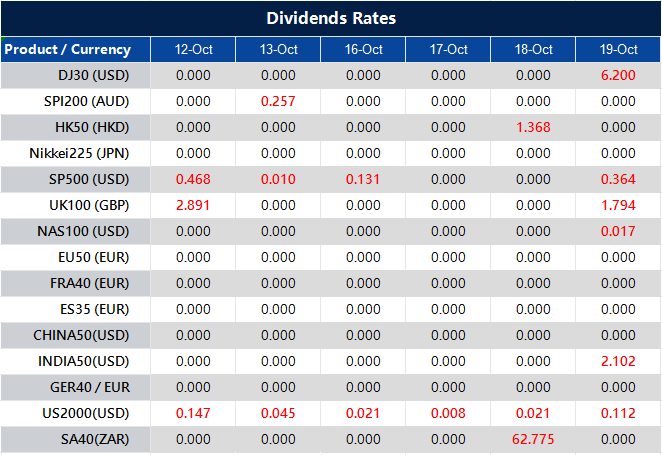

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

On Monday, the stock market surged as traders eagerly awaited corporate earnings reports, pushing the Dow Jones Industrial Average to its best day since September. Despite concerns about rising Treasury yields, oil prices, inflation, and conflicts in the Middle East, investors were focusing on earnings reports, offering short-term optimism. The US dollar faced a decline due to geopolitical tensions, while the British pound rose, reflecting increased risk appetite. Meanwhile, the currency market monitored the USD/JPY pair and the movements in Treasury-JGB yield spreads, with expectations of higher interest rates driving the push towards a significant breakout at 150. Additionally, the Aussie, Kiwi, and Polish zloty all saw gains.

Stock Market Updates

On Monday, the stock market saw a positive surge as traders eagerly anticipated a wave of corporate earnings reports, seemingly unfazed by an increase in Treasury yields. The Dow Jones Industrial Average experienced its best day since September, climbing 314.25 points, or 0.93%, to close at 33,984.54. Likewise, the S&P 500 recorded a 1.06% gain, ending the day at 4,373.63, and the Nasdaq Composite rose by 1.2% to reach 13,567.98. Leading the Dow’s ascent were Nike and Travelers Companies, both posting gains of approximately 2.1%, while all 11 S&P 500 sectors traded higher during the session. Earnings season was set to intensify, with 11% of the S&P 500 slated to report results, including notable names like Johnson & Johnson, Bank of America, Netflix, and Tesla. A focus on earnings reports was offering investors optimism in the short term, amid concerns about rising yields, oil prices, inflation, and conflicts in the Middle East.

Although the previous week had been marked by mixed performance in the stock market, with the S&P 500 experiencing a 0.5% gain for its second consecutive positive week and the Dow gaining 0.8%, it appeared that the market was beginning to normalize after reacting to geopolitical surprises. Despite potential volatility into the year’s end, investors were increasingly focusing on the fundamentals and corporate performance as the market appeared to adapt to recent uncertainties in the geopolitical landscape.

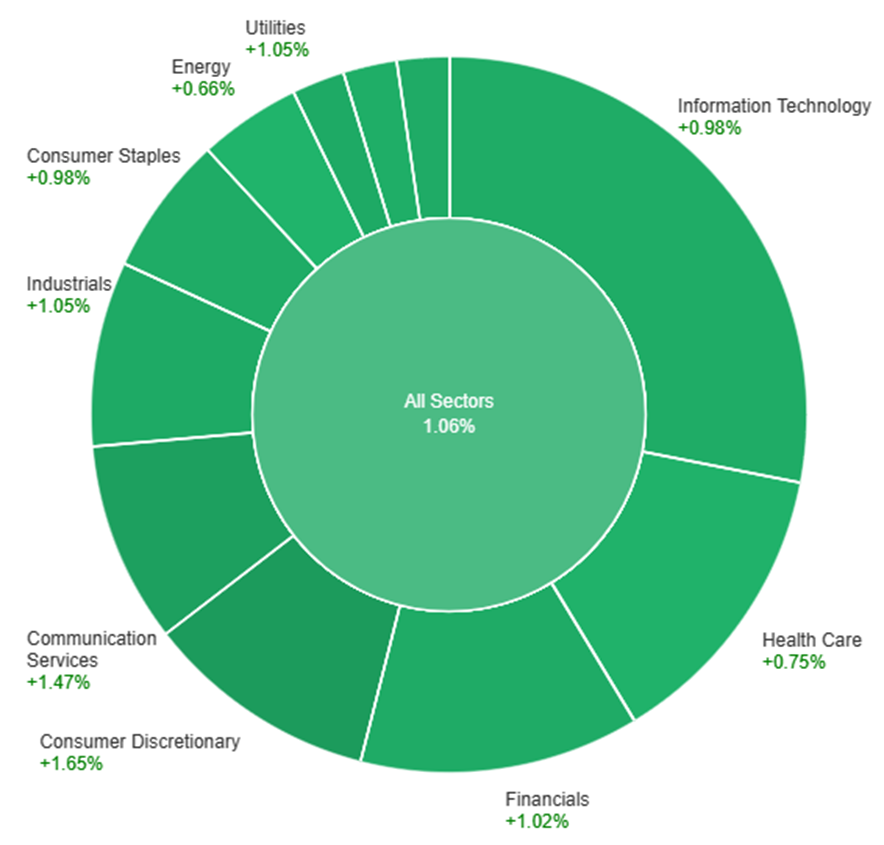

On Monday, across all sectors, the market experienced a positive trend with an overall increase of 1.06%. The highest gains were observed in the Consumer Discretionary sector, which saw a rise of 1.65%, followed by Communication Services at 1.47%, and Industrials at 1.05%. Other sectors also saw positive but relatively smaller gains, such as Utilities, Real Estate, Financials, Consumer Staples, Information Technology, Materials, Health Care, and Energy, with increases ranging from 0.66% to 0.98%.

Currency Market Updates

In the currency market, the US dollar faced a decline of 0.37% as part of a broader retreat triggered by widespread derisking flows, largely connected to the Israel-Hamas conflict. This geopolitical tension had previously bolstered the US dollar late in the previous week. Despite a slight dip in bund-Treasury yield spreads, the EUR/USD pair managed to rise by 0.4% during this period, as demand for the safe-haven US dollar diminished. Notably, this surge came after eleven consecutive weeks of losses for the EUR/USD pair, a trend potentially signaling an oversold condition. It was also noted that the market sentiment had shifted, with expectations of the Federal Reserve halting its interest rate hikes.

On a similar note, the British pound (GBP) witnessed a 0.55% rise, benefiting from increased risk appetite and wider gilts-Treasury yield spreads. Huw Pill, the Chief Economist of the Bank of England (BoE), issued a warning against prematurely declaring victory over inflation. Sterling traders were anticipating the release of UK inflation data, with market expectations leaning towards the BoE being the sole major central bank likely to implement rate hikes. This expectation effectively ruled out the possibility of a UK rate cut until late 2024. Meanwhile, the USD/JPY pair remained relatively unchanged, lingering below the peak observed in October 2023 at 150.165 and the significant resistance point at 151.94, which had last been reached in 2022. The market was closely monitoring the movements in Treasury-JGB yield spreads, as they played a pivotal role in the carry trade dynamics of the currency pair. Strong US retail sales and other data that fueled expectations of higher interest rates from the Federal Reserve appeared to be the key factor driving the push towards a significant breakout at 150, with 151.94 serving as a major resistance level. Additionally, the absence of Japanese foreign exchange intervention was a critical piece of the puzzle in this scenario. Amid these developments, the Australian and New Zealand dollars, colloquially known as the Aussie and Kiwi, rose by approximately 0.7% as risk appetite rebounded in the market. Furthermore, the Polish zloty witnessed a remarkable increase of 2.2% following weekend election results that were perceived as likely to lead to improved relations within the European Union (EU).

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Edges Higher Amid Middle East Tensions and Economic Uncertainty

The EUR/USD pair saw a slight uptick, reaching 1.0554 on Monday as it closed trading below this peak. A stronger US Dollar at the start of the week, driven by ongoing Middle East tensions, initially led to a demand for safety. However, as the day progressed, the USD weakened against major currencies. The escalating conflict in the Middle East, marked by attacks from Hezbollah in addition to the ongoing Israel-Palestine conflict, created global economic uncertainty and added pressure on central banks. Data releases were limited, with Germany’s Wholesale Price Index edging up, the Euro Zone showing an improved trade balance, and the US reporting a decline in the NY Empire State Manufacturing Index. Upcoming releases include Germany’s ZEW Survey on Economic Sentiment and US Retail Sales for September, Industrial Production, Capacity Utilization, and Business Inventories for August.

Based on technical analysis, the EUR/USD was slightly higher on Monday, pushing towards the middle band of the Bollinger Bands. Currently, the EUR/USD is trading at the middle band, suggesting the potential for a consolidating move. The Relative Strength Index (RSI) stands at 48, indicating that the EUR/USD is back to neutral bias.

Resistance: 1.0560, 1.0616

Support: 1.0502, 1.0451

XAU/USD (4 Hours)

XAU/USD Faces Volatility Amid Geopolitical Tensions and Fragile Market Sentiment

Spot Gold, represented as XAU/USD, started the week with a gap lower, retreating from a recent multi-week high. Geopolitical concerns in the Middle East, particularly the escalating conflict between Israel and Hamas, kept financial markets on edge. However, the demand for the US Dollar decreased during European trading hours, allowing XAU/USD to recover around the $1,920 price range. While US stock markets posted gains, the market sentiment remains delicate due to uncertainty in the economic outlook and future monetary policies. Major central banks have paused tightening, but the potential for additional rate hikes lingers, given persistent inflationary pressures. This week’s inflation reports from New Zealand, Canada, and the UK will play a crucial role in determining the precious metal’s performance in the face of mounting price pressures.

Based on technical analysis, XAU/USD is moving slightly lower on Monday and consolidating between the upper and middle bands of the Bollinger Bands. Currently, the price of gold is still moving near the support level with the potential of moving lower. The Relative Strength Index (RSI) currently registers at 66, indicating a bullish bias for the XAU/USD pair.

Maserati MSG Racing and VT Markets announce new partnership in Formula E

Two Giants Unite

As Season 10 of the FIA Formula E World Championship fast-approaches, Maserati MSG Racing is proud to announce a multi-year global partnership with VT Markets, a leading online broker in the financial space.

Marking one of the first collaborations of its kind in the Forex landscape — and VT Markets’ first sporting partnership — the move sees two industry giants unite as both the motorsport and financial sectors join forces.

The Power of Opportunity

In an industry saturated by competition, VT Markets has broken from the pack and is accelerating into the future with its customers in mind by making trading more accessible for all.

Like Maserati MSG Racing, VT Markets believes in the power of opportunity and advancement. By leveraging and coupling constant innovation with best-in-class service standards, the brokerage continues to break new ground by successfully simplifying a once complex trading process.

Since its launch in 2015, VT Markets has facilitated new opportunities by allowing everyday traders to enjoy a smooth, stress-free experience, both online and on its award-winning mobile app.

The Race for a Better Tomorrow

Maserati MSG Racing is delighted to welcome VT Markets to the world of Formula E. Following a successful Season 9 — which yielded four podiums and the Maserati brand’s first victory in World Championship single-seaters since 1957 — the team has its sights firmly set on further glory in Season 10.

United by a shared belief in uncompromising performance and technical innovation, Maserati MSG Racing and VT Markets will forge their bond in Formula E to create and safeguard an environmentally and socially sustainable future.

Alongside racing together with a common purpose, VT Markets’ branding will feature on the cars and race suits of drivers Maximilian Günther and Jehan Daruvala, in the team’s garage, and across teamwear in Season 10.

Pre-season testing for Formula E’s 2023/24 campaign will take place at Valencia’s Circuit Ricardo Tormo from 23–27 October ahead of the series’ season-opening race in Mexico City on 13 January, 2024.

In Their Words

Scott Swid, Chairman & Managing Partner, Maserati MSG Racing

“We are very pleased to welcome VT Markets to the Maserati MSG Racing family. Our partners are an integral part of our family and they play a critical role in our journey. Coming from the fast-paced world of finance, VT Markets fully understands our relentless pursuit of performance excellence in Formula E, and our shared passion for technical innovation will make for a dynamic, exciting, and hopefully rewarding journey together from Season 10 onwards.”

Harry Richards, Commercial Director, Maserati MSG Racing

“Season 10 is a very exciting time to be a part of Formula E, and we’re delighted to welcome VT Markets to Maserati MSG Racing. Since its inception in 2014, Formula E has carved out a unique position in the motorsport landscape and has become a go-to destination for premium global brands to showcase their vision. Innovation is at the heart of what we do as a racing team, and so to attract like-minded partners, who share and believe in our mission, is in an integral part of our journey. We’re all very excited to work with VT Markets this coming season, and we can’t wait to see what we can achieve together.”

Chief Executive Officer, VT Markets

“This partnership between VT Markets and Maserati MSG Racing represents a unique convergence of two leading brands in their respective fields. While the industries might differ, both organisations are remarkably aligned in their commercial ambitions and vision for the world. The Maserati Trident has long been a distinctive symbol of quality and prestige, and we’re delighted to move into the future alongside partners of such repute.”

About VT Markets:

VT Markets is a regulated multi-asset broker with a presence in over 160 countries. To date, it has won numerous international accolades including Best Customer Service and Fastest Growing Broker.

In line with its mission to make trading accessible to all, VT Markets currently offers unfettered access to over 1,000 financial instruments and a secure, seamless trading experience via its award-winning mobile app.

For media enquiries and sponsorship opportunities, please email media@vtmarkets.com.

Maserati MSG Racing Maserati MSG Racing is one of the founding teams of the FIA Formula E World Championship and in December 2013, became the first manufacturer to join motorsport’s premier fully-electric category. As one of only a handful of constant participants since the series’ inaugural 2014/15 season, MSG Racing has moved from strength to strength and tasted vice World Championship success in 2021 before completing its most successful season to date in 2022, finishing the campaign as the vice World Teams’ Champions.

Let by Chairman & Managing Partner, Scott Swid, and Team Principal, James Rossiter, the Monégasque marque is at the forefront of sustainability, EDI, technical innovation, and excellence. For further information, visit our website. For media hub access and rights-free content, please register here.

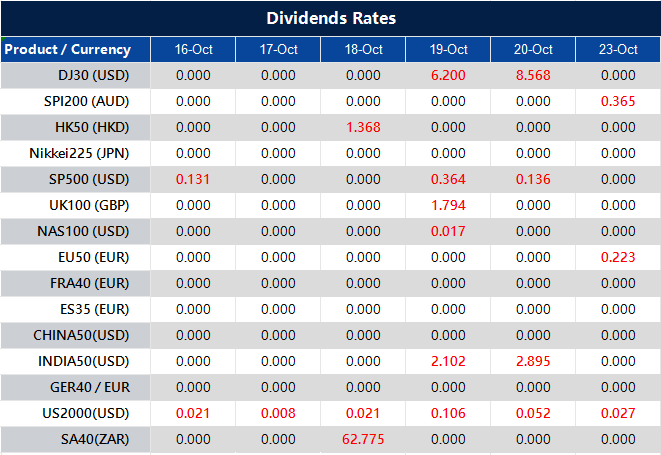

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Traders should keep a close eye on US retail sales and the Consumer Price Index (CPI) reports from New Zealand, Canada, and the UK this week, as these updates could have a substantial influence on the market. Exercise caution and stay up to date with the latest developments to ensure a successful week of trading.

Here are some notable market highlights for the upcoming week:

New Zealand Consumer Price Index (17 October 2023)

In Q2 2023, the CPI for New Zealand increased by 1.1%.

The CPI data for Q3 is set to be released on 17 October, with analysts anticipating a 1.9% increase.

UK Claimant Count Change (17 October 2023)

The number of people claiming unemployment benefits in the UK increased by 900 in August 2023.

An additional increase of 22,000 is anticipated in the upcoming data, due for release on 17 October.

Canada Consumer Price Index (17 October 2023)

Canada’s CPI rose by 0.4% in August 2023 compared to the previous month.

Analysts expect a 0.1% increase in the September figures, which are scheduled for release on 17 October.

US Retail Sales (17 October 2023)

US retail sales saw a month-over-month increase of 0.6% in August 2023, surpassing the 0.5% uptick recorded in July 2023.

Analysts anticipate a 0.3% increase in the data for September, set to be released on 17 October.

UK Consumer Price Index (18 October 2023)

CPI in the UK eased to 6.7% in August 2023 from 6.8% in the previous month, the lowest rate since February 2022.

CPI figures for the next reporting period are expected to further decrease to 6.5%.

Employment in Australia (19 October 2023)

Employment in Australia increased by 64,900 in August 2023, while the unemployment rate stood at 3.7%.

Analysts anticipate that the employment figures for September 2023 will reflect an increase of 20,900 jobs, with the unemployment rate expected to remain at 3.7%. This data is scheduled for release on 19 October.

UK Retail Sales (20 October 2023)

Retail sales in the UK rose by 0.4% in August 2023, partially recovering from a 1.1% decline in July.

The next set of data will be released on 20 October, with analysts expecting a decrease of 0.3%.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

On Thursday, the stock market faced a decline driven by concerns over rising Treasury yields and persistent US inflation, marking the end of a four-day winning streak for major indexes. The Dow Jones Industrial Average dropped 0.51%, while the S&P 500 and Nasdaq Composite fell by 0.62% and 0.63%, respectively. Meanwhile, the US Dollar rallied by 0.80% as robust economic data and increased Treasury yields reinforced expectations of prolonged high interest rates. European currencies, such as the Euro and British Pound, experienced declines, while precious metals like Gold and Silver slipped due to rising Treasury yields. Geopolitical concerns, including the Israel-Hamas conflict, also contributed to market sentiment.

Stock Market Updates

Stocks experienced a decline on Thursday due to concerns about rising Treasury yields and persistent U.S. inflation. The Dow Jones Industrial Average closed 0.51% lower, dropping 173.73 points to 33,631.14, while the S&P 500 fell by 0.62%, finishing at 4,349.61, and the Nasdaq Composite lost 0.63%, closing at 13,574.22. This decline marked the end of a four-day winning streak for the major indexes. Treasury yields surged with the 10-year rate increasing by nearly 11 basis points to 4.70%, while the 2-year Treasury yield reached 5.06% after rising more than 6 basis points. Many investors believe that higher yields are becoming a permanent feature, which influenced the equity market’s downturn. The consumer price index released on Thursday revealed a 0.4% increase on the month and a 3.7% increase from a year ago, exceeding Dow Jones estimates of 0.3% and 3.6%, respectively.

In corporate news, Walgreens saw its shares trade 7% higher after reporting narrower losses and progress in cost-cutting plans, although it offered soft profit guidance and missed earnings expectations. Additionally, several major companies, including JPMorgan, BlackRock, and UnitedHealth Group, are scheduled to report earnings on Friday. Geopolitical concerns also played a role in market sentiment, as the ongoing Israel-Hamas conflict raised questions about a potential oil supply crunch and a subsequent increase in fuel prices should the instability spread to neighboring oil-producing regions.

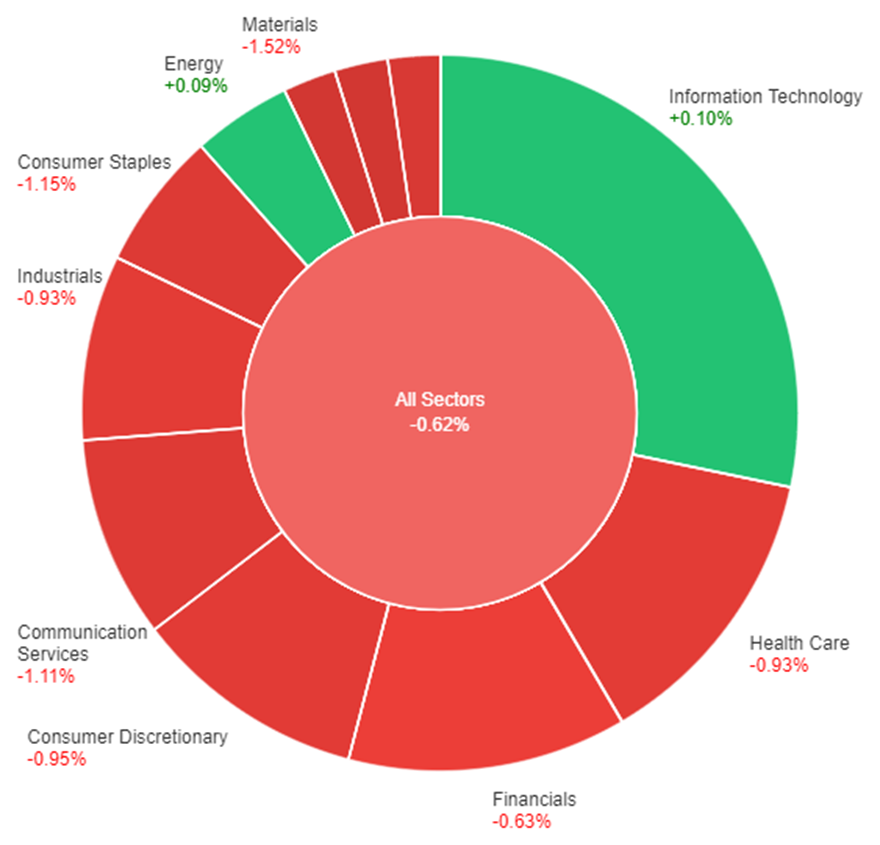

On Thursday, across all sectors, the overall market saw a decline of 0.62%. The Information Technology sector performed the best with a modest gain of 0.10%, while Energy followed closely with an increase of 0.09%. On the other hand, the Utilities sector experienced the most significant drop, with a decline of 1.50%. Additionally, Real Estate, Consumer Staples, and Materials sectors also saw notable decreases, declining by 1.31%, 1.15%, and 1.52%, respectively. The Financials, Health Care, Industrials, Consumer Discretionary, and Communication Services sectors all recorded losses ranging from 0.63% to 1.11%.

Currency Market Updates

The US Dollar exhibited a significant rally, recovering from previous losses but still below recent cycle peaks. The US Dollar index surged by 0.80% to reach 106.55, primarily propelled by robust US economic data and increased Treasury yields. In September, the US annual Consumer Price Index (CPI) exceeded expectations, registering at 3.7%, surpassing the market consensus of 3.6%. The Producer Price Index (PPI) also outperformed expectations, and Initial Jobless Claims remained slightly below the consensus, at 209,000. This series of strong US economic data and the persistence of inflation above target levels reinforced expectations of prolonged high interest rates. Analysts noted that the Federal Reserve is likely to remain patient as it assesses the overall data, with the focus on the upcoming November FOMC meeting. Meanwhile, US Treasury yields experienced an increase, with the 10-year yield rising from 4.57% to 4.73%, and the 2-year yield from 4.98% to 5.07%.

In the currency markets, the Euro (EUR/USD) saw a significant decline to 1.0525 from around 1.0630 due to the strengthening US Dollar, driven by the robust economic data. Europe is awaiting the release of Industrial Production data for August and an appearance by European Central Bank (ECB) President Lagarde at the annual International Monetary Fund and World Bank meeting. The British Pound (GBP/USD) ended its six-day positive streak, recording a 140-pip drop below 1.2200 amid negative risk sentiment. The New Zealand Dollar (NZD/USD) declined for the second consecutive day, falling below 0.6000 and the 20-day Simple Moving Average (SMA) to reach 0.5925. New Zealand is poised to release Electronic Card Retail Sales data and the Business NZ PMI for September. The Australian Dollar (AUD/USD) posted one of its lowest daily closes for the year, hovering slightly above 0.6300, with a downward bias and attention on the October lows at 0.6285. Meanwhile, the Canadian Dollar (USD/CAD) strengthened, approaching 1.3700 on the back of US Dollar strength, with a potential target of 1.3800 if it closes above 1.3750. Precious metals like Gold and Silver faced declines due to the rise in Treasury yields, with Gold slipping below $1,870 and Silver dropping beneath $22.00. Upcoming data releases from China and Europe, as well as the University of Michigan Consumer Sentiment survey, hold the potential to impact these currency markets, especially those of the antipodean currencies.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Slides to 1.0520 as Stronger US Dollar, Rising Yields Pressure Pair

The EUR/USD pair dipped from weekly highs above 1.0630 to 1.0520, driven by a stronger US Dollar bolstered by higher Treasury yields and encouraging US economic data. The European Central Bank’s recent meeting minutes revealed support for a potential interest rate hike, though this had a limited impact on the Euro. Meanwhile, the US Dollar gained further momentum following a 0.4% rise in the Consumer Price Index (CPI) for September, adding to expectations of prolonged higher interest rates. With the 10-year yield surging to 4.72%, the Greenback’s correction ended, leaving it poised to challenge cycle highs.

Based on technical analysis, the EUR/USD fell on Thursday, pushing towards the lower band of the Bollinger Bands. Currently, the EUR/USD is trading around the lower band, while the bands are trending upwards, suggesting the potential for consolidating move to retest the middle Bollinger Band. The Relative Strength Index (RSI) stands at 42, indicating that the EUR/USD is back to netural bias.

Resistance: 1.0582, 1.0640

Support: 1.0520, 1.0460

XAU/USD (4 Hours)

XAU/USD Dip as Hawkish Fed Sentiment Surges on Strong US CPI Data

Investors are reevaluating their expectations for the US Federal Reserve as robust Consumer Price Index (CPI) data, revealing a 0.4% increase last month and an annual inflation rate of 3.7% in September, further strengthens the narrative of “higher rates for longer.” This has boosted the US Dollar and Treasury bond yields, causing Gold prices to retreat from their recent two-week high above $1,880 and dip below $1,870. The surge in hawkish Fed sentiments is fueling uncertainty, with markets now placing a 38% probability of a December rate hike, compared to the previous 28%. In addition, softer Chinese CPI and Producer Price Index data are contributing to risk aversion. As we await US Consumer Sentiment and Inflation Expectations data, along with speeches from Fed policymakers, the future of the US Dollar remains uncertain.

Based on technical analysis, XAU/USD is moving slightly lower on Thursday and able to reach the middle band of the Bollinger Bands. Currently, the price of gold is trading slightly above the middle band with the potential of moving back higher. The Relative Strength Index (RSI) currently registers at 62, indicating a bullish bias for the XAU/USD pair.

The Landscape of Forex Trading in The United Kingdom

The foreign exchange (Forex) arena is a magnet for global traders, with the UK emerging as a pivotal hub. Over the last ten years, the momentum around Forex trading in the UK has intensified. From seasoned professionals to enthusiastic novices, understanding the dynamics of the UK Forex scene is pivotal.

Highlighting the UK’s prominence in the global Forex market, recent statistics shed light on its trading volumes and market share, illustrating the country’s key role in Forex trading dynamics.

Snapshot of the Forex World

Forex trading revolves around purchasing one currency while offloading another, capitalizing on currency value fluctuations for gains. Clocking a daily turnover north of $6 trillion, the global Forex market sits atop the financial hierarchy.

The UK survey findings are outlined as follows:

In April 2022, the daily average transaction volume in theUK’s foreign exchange market reached $3,755 billion, marking an increase from the $3,576 billion daily volume recorded in April 2019.

Despite witnessing a decline from 43.2% in April 2019 to 38.1% in global turnover by 2022, the UK continues to hold its position as the predominant hub for foreign exchange activities. This 2022 figure aligns with the UK’s market share as observed in earlier surveys.

Over-the-counter (OTC) interest rate derivatives had an average daily turnover of $2,626 billion in April 2022, showing a drop from the $3,670 billion noted in April 2019.

The UK dominated the OTC interest rate derivatives market in April 2022, representing 45.5% of the global turnover. This is a slight decrease from the 50.6% market share in April 2019. Despite seeing reduced activity in major centres, including the US, since the 2019 survey, the UK sustains its lead in this domain. The market share in the 2022 survey aligns with most of the past records, with the exception of a significant dip in 2016.

Over-the-counter (OTC) refers to the process of trading financial instruments directly between two parties outside of formal exchanges, providing a more flexible and personalized trading environment.

The UK’s appeal as a central Forex destination is in no small part due to its stringent regulatory environment. The UK’s Financial Conduct Authority (FCA) oversees the Forex sphere, mandating brokers to follow rigorous norms for trader safety. Collaborating with an FCA-compliant broker translates to enhanced peace of mind for traders.

Why Forex Trading is Popular in The UK?

Forex trading is popular in the UK for several reasons. The country boasts a well-established financial infrastructure, particularly in London, which serves as a global financial hub. This allows traders access to advanced technology, fast execution speeds, and a diverse range of brokers. The UK’s FCA-regulated environment provides security and trust, ensuring that traders are protected. Additionally, the UK’s strategic time zone allows traders to engage with the Asian, European, and US markets throughout the day, increasing opportunities for profitable trades. The tax-free spread betting option further adds to its appeal for traders.

Advantages of Forex Trading in the UK

State-of-the-Art Infrastructure: Particularly in London, the UK prides itself on its avant-garde technology and infrastructure, setting the stage for optimal Forex operations.

Varied Trading Windows: The UK’s strategic position means traders can engage with Asian markets at dawn, European zones mid-day, and US circuits by dusk.

Extensive Broker Options: The UK is home to a plethora of premium Forex brokers, catering to a spectrum of trader proficiencies.

Tax Incentives: In the UK, spread betting—a Forex variant—is exempt from taxes, enhancing its allure for traders.

What To Take Note Of When Trading FX in The UK

When trading Forex in the UK, it’s essential to consider a few key factors. First, ensure you’re working with an FCA-regulated broker for security and transparency. Be mindful of market volatility, as the Forex market can experience sharp price swings that may lead to significant losses if not managed well. Leverage is another important consideration, as it can magnify both profits and losses. Stay updated on global economic and political events, as these can impact currency values. Lastly, take advantage of the UK’s tax-free spread betting options.

Forex Trading Challenges

Unpredictability: Forex markets are notoriously unpredictable. High returns are possible, but so are considerable losses.

The Leverage Double-Edged Sword: Numerous brokers proffer significant leverage, enabling traders to helm expansive positions with minimal capital. This can boost gains, but losses too.

Intricacy: Grasping the intricacies of Forex necessitates understanding of the macroeconomic landscape and global geopolitics.

Beginners Starting Their Journey In The UK

Beginners starting their Forex journey in the UK should focus on building a strong foundation. It’s crucial to understand the basics of Forex trading, including how the market operates, key terms, and trading strategies. Using a demo account is highly recommended for practicing without risking real money. Beginners should also ensure they choose an FCA-regulated broker for added security. Staying updated on economic news and learning to manage risk effectively through tools like stop-loss orders will help build confidence and long-term trading success.

Prioritize Learning: Dive into comprehensive research on the Forex market, trading blueprints, and risk mitigation before initiating.

Kick-off with a Practice Account: Use a demo account to hone your skills sans real monetary stakes.

Stay Updated: Continuously monitor international news, economic developments, and other currency influencers.

Embrace Risk Management: Leverage tools like stop-loss and take-profit orders to curtail risks and secure gains.

Use Leverage Wisely: Understand the risks of leverage and use it cautiously to avoid significant losses.

Broker Selection is Critical: Opt for reliable Forex brokers who align with your trading objectives.

Wrapping Up

The UK Forex market offers vast opportunities for traders, backed by strong regulatory oversight from the FCA and advanced financial infrastructure. However, to succeed, you need more than just access—you need informed strategies, a thorough understanding of market dynamics, and careful risk management. Whether you’re a seasoned trader or just starting out, the right tools, broker selection, and continuous learning are key to navigating the UK’s ever-changing Forex landscape. By being prepared and staying updated, you’re well-positioned for long-term success.

Why Choose VT Markets For Forex Trading in the UK

Choosing VT Markets gives you access to advanced trading platforms suitable for all experience levels, competitive spreads, and a broad range of currency pairs. With fast execution speeds and top-tier security standards, VT Markets ensures a seamless trading experience. Plus, our comprehensive educational resources and dedicated customer support help you grow and succeed in the Forex market.

Start your trading journey with VT Markets today and unlock the tools you need to trade confidently and profitably!

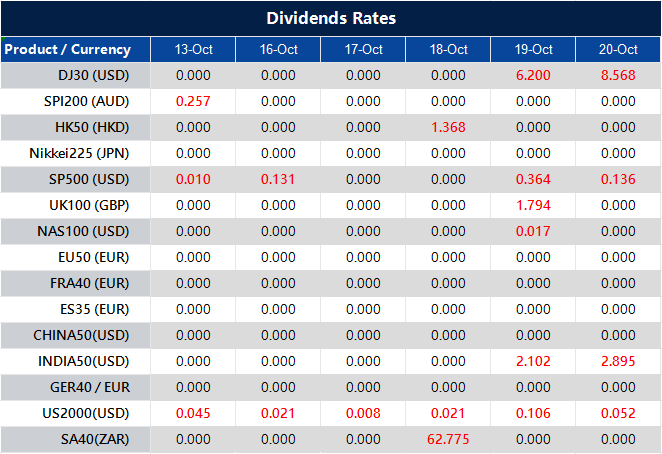

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Major stock indices, including the Dow Jones Industrial Average, S&P 500, and Nasdaq Composite, saw modest gains as investors awaited U.S. consumer inflation figures and monitored Treasury yields’ retreat. The market was also influenced by expectations of the consumer price index report and Federal Reserve policy, while Exxon Mobil announced a significant acquisition and Birkenstock faced a challenging market debut. Geopolitical tensions in Israel and Hamas contributed to market uncertainty. In the currency market, the US Dollar remained flat despite positive wholesale inflation data and FOMC minutes, with the focus shifting to the impending Consumer Price Index release and divergent views among committee members. The US Dollar Index and Treasury yields experienced minor fluctuations, while currency pairs like EUR/USD and GBP/USD demonstrated varied behavior. Gold and Silver rallied due to lower yields and a weakened US Dollar.

Stock Market Updates

In Wednesday’s stock market, major indices saw modest gains as investors eagerly awaited the release of the new U.S. consumer inflation figures, while Treasury yields continued their retreat. The Dow Jones Industrial Average rose by 0.19%, or 65.57 points, closing at 33,804.87. The S&P 500 experienced a 0.43% increase, ending the day at 4,376.95, while the Nasdaq Composite, dominated by tech stocks, surged 0.71% and closed above its 50-day moving average for the first time since September 14. This marked the fourth consecutive day of gains for these key indices. Investors were also anticipating the consumer price index report for September, with economists predicting a 0.3% increase from the previous month and a year-over-year rise of 3.6%. This data was seen as critical for insights into future Federal Reserve policy moves, especially after the recent revelation of hotter-than-expected wholesale inflation figures. Additionally, the release of minutes from the Fed’s September meeting indicated that a majority of officials believed one more interest rate hike was likely, with rising Treasury yields playing a significant role in their considerations.

On the corporate front, Exxon Mobil announced the acquisition of shale driller Pioneer Natural Resources in an all-stock deal worth $59.5 billion, marking the largest merger announced on Wall Street in the year. Meanwhile, sandal manufacturer Birkenstock faced a challenging market debut, with shares priced at $46 each but falling to $40.20 by the close of the session. Investors were also monitoring the ongoing conflict between Israel and Hamas, as the latter launched an attack on Israeli civilians, leading to the deadliest offensive in the region in five decades. President Joe Biden condemned the attacks as terrorism and expressed unwavering support for Israel. Overall, the market sentiment appeared uncertain, with conflicting factors such as inflation, interest rates, and geopolitical tensions contributing to the mixed outlook for stocks.

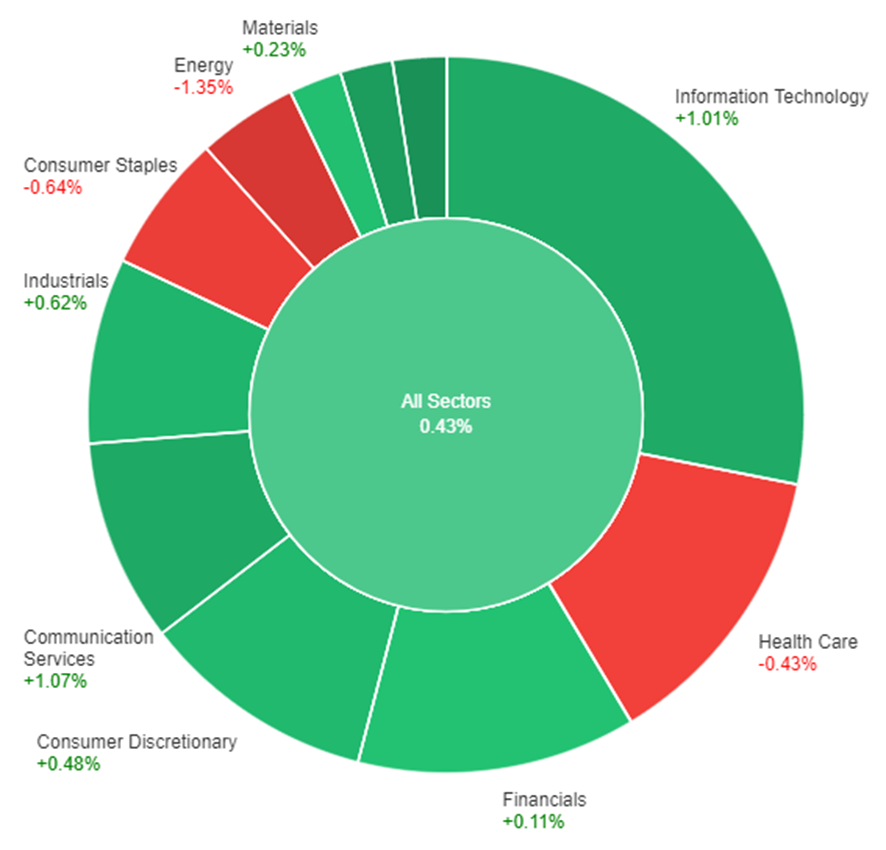

On Wednesday, the performance of various sectors in the market showed mixed results. Overall, all sectors combined saw a modest increase of 0.43%. Among the sectors, Real Estate performed exceptionally well with a gain of 2.01%, followed by Utilities at 1.63%, and Communication Services at 1.07%. Information Technology and Industrials also had positive gains at 1.01% and 0.62%, respectively. Meanwhile, Consumer Discretionary and Materials had smaller gains at 0.48% and 0.23%. On the other hand, Financials and Health Care experienced minimal gains of 0.11% and a decline of -0.43%, respectively. Consumer Staples and Energy were the worst-performing sectors, with losses of -0.64% and -1.35%, respectively.

Currency Market Updates

In the recent currency market updates, the US Dollar remained largely flat despite unexpected positive data on US wholesale inflation and the release of the Federal Open Market Committee (FOMC) minutes. The Greenback’s weakness persisted as US Treasury yields continued to retreat, and a risk-on sentiment in the Wall Street stock market failed to provide support. Notably, the US Producer Price Index (PPI) accelerated in September, surprising analysts by rising from 2.0% to 2.2%, as compared to the expected 1.6%. However, this development did not raise significant concerns, with all eyes turning to the impending release of the Consumer Price Index (CPI), expected to decrease from 3.7% to 3.6% in September, promising heightened volatility in the currency market. Furthermore, the FOMC minutes revealed divergent perspectives among committee members, emphasizing a data-dependent approach and the necessity of a substantial rebound in inflation to reach a consensus on further interest rate hikes.

Following the FOMC minutes, the US Dollar Index (DXY) experienced a slight pullback but managed to finish flat at 105.75, rebounding from strong support at 105.50. The US Treasury yield for 10-year bonds dropped to 4.55%. Notably, EUR/USD maintained its recent gains and stayed close to a strong resistance level at 1.0630, demonstrating a bullish tone. However, with a week of continuous ascent, the pair appeared poised for a consolidation phase, pending the release of the US CPI figures. Meanwhile, GBP/USD achieved a second consecutive daily close above the 20-day Simple Moving Average, hovering around 1.2300 and indicating signs of potential fatigue in its recovery. Key economic data releases are expected in the UK on Thursday. In addition, Gold and Silver rallied, benefiting from lower yields and a weakened US Dollar, breaking above $1,860 and $22.00, respectively.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Rebounds from Monthly Lows Amidst Weakening US Dollar and Data-Dependent Fed Stance

The EUR/USD pair tested levels above 1.0630 before pulling back, displaying modest gains as it recovers from monthly lows. Trading in a critical area, the Euro awaits more US inflation data, benefiting from the US Dollar’s weakness due to declining yields and positive market sentiment. The unexpected rise in the US Producer Price Index didn’t significantly impact the Dollar, while the latest FOMC minutes highlighted the Fed’s data-dependent approach to policy. A busy economic calendar on Thursday includes the release of ECB minutes and the US Consumer Price Index, with potential market impact depending on the CPI’s performance.

Based on technical analysis, the EUR/USD rose on Wednesday, pushing towards the upper band of the Bollinger Bands. Currently, the EUR/USD is trading below the upper band, while the bands are trending upwards, suggesting the potential for another upward move to retest the upper Bollinger Band. The Relative Strength Index (RSI) stands at 62, indicating that the EUR/USD is currently attempting to establish a bullish bias.

Resistance: 1.0674, 1.0736

Support: 1.0583, 1.0530

XAU/USD (4 Hours)

XAU/USD Surges to Two-Week High Amidst US Dollar Weakness and Bond Yield Concerns

In a strong rally, the price of gold (XAU/USD) soared to a fresh two-week high at $1,877.19 per troy ounce on Wednesday. This impressive surge was attributed to the widespread weakness of the US Dollar, which was in turn linked to declining US Treasury bond yields. The dip in yields was partially driven by renewed demand for safety amid Middle East developments and dampened expectations of another Federal Reserve rate hike, as policymakers generally anticipate that robust yields will obviate the need for further tightening. Nevertheless, even as yields have eased lately, they remain near the multi-decade highs observed in September. Investor sentiment became cautious after the release of the US Producer Price Index (PPI) and in anticipation of the FOMC Meeting Minutes, as wholesale inflation in the country surged by 2.2% YoY in September, exceeding market expectations and August figures. The release of the Consumer Price Index (CPI) on Thursday is anticipated to show a 3.6% YoY increase, further influencing the gold market.

Based on technical analysis, XAU/USD is trending higher on Wednesday, creating an uptrend within the Bollinger Bands. Currently, the price of gold is trading slightly below the upper band and is beginning to consolidate between the middle and upper bands of the Bollinger Bands. The Relative Strength Index (RSI) currently registers at 75, indicating a bullish bias for the XAU/USD pair.