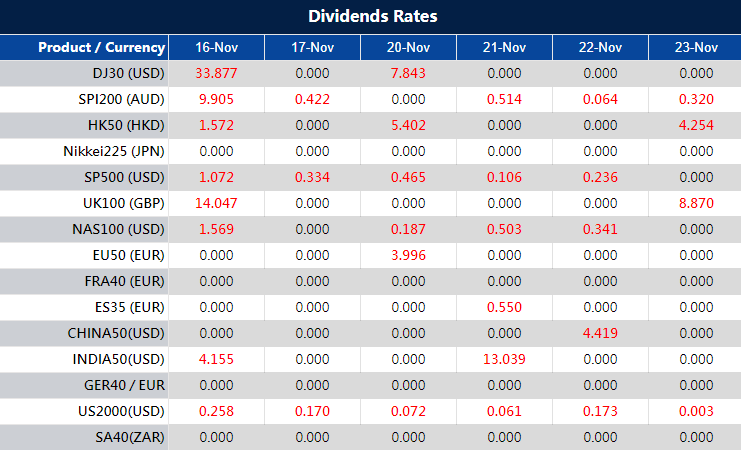

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Written on November 16, 2023 at 7:42 am, by anakin

After positive inflation data, stock markets continued their climb, marked by modest gains in the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average. However, despite a notable drop in the producer price index, retail sales declined, painting a mixed economic picture. Corporate highlights included Target’s 18% surge on strong Q3 results and V.F. Corp’s 14% rise post-JPMorgan’s upgrade. Currency markets saw the US dollar rebound after strong retail sales, influencing US Treasury yields and readjusting rate-cut forecasts. EUR/USD faced resistance, while USD/JPY surged and GBP/USD declined amidst varied economic data. Commodity-linked currencies like CAD and AUD held steady amid global growth expectations and the dollar’s resurgence despite falling oil prices.

Stock Market Updates

Wednesday saw stocks maintaining their upward momentum after favorable inflation data. The S&P 500 inched up by 0.16%, reaching 4,502.88 at closing, and the Nasdaq Composite recorded a slight 0.07% rise, closing the day at 14,103.84. The Dow Jones Industrial Average climbed by 0.47%, gaining 163.51 points to close at 34,991.21. The 10-year U.S. Treasury yield rose by 9 basis points, reaching 4.537%, rebounding after slipping below 4.5% previously.

October’s producer price index, a measure of wholesale prices, experienced its most significant drop since April 2020, decreasing by 0.5%. However, retail sales also declined, presenting a mixed picture of economic data. These movements followed a strong prior session triggered by the consumer price index remaining flat for October, contrary to expectations of a slight increase.

In the corporate world, Target’s stocks surged almost 18% after surpassing third-quarter expectations, while V.F. Corp’s shares rose 14% post an upgrade from JPMorgan. Meanwhile, the focus shifted to Washington as lawmakers aimed to avert a government shutdown. The House of Representatives passed a bill for a “laddered” continuing resolution, moving it to the Senate for a vote to avoid a potential federal shutdown by week’s end.

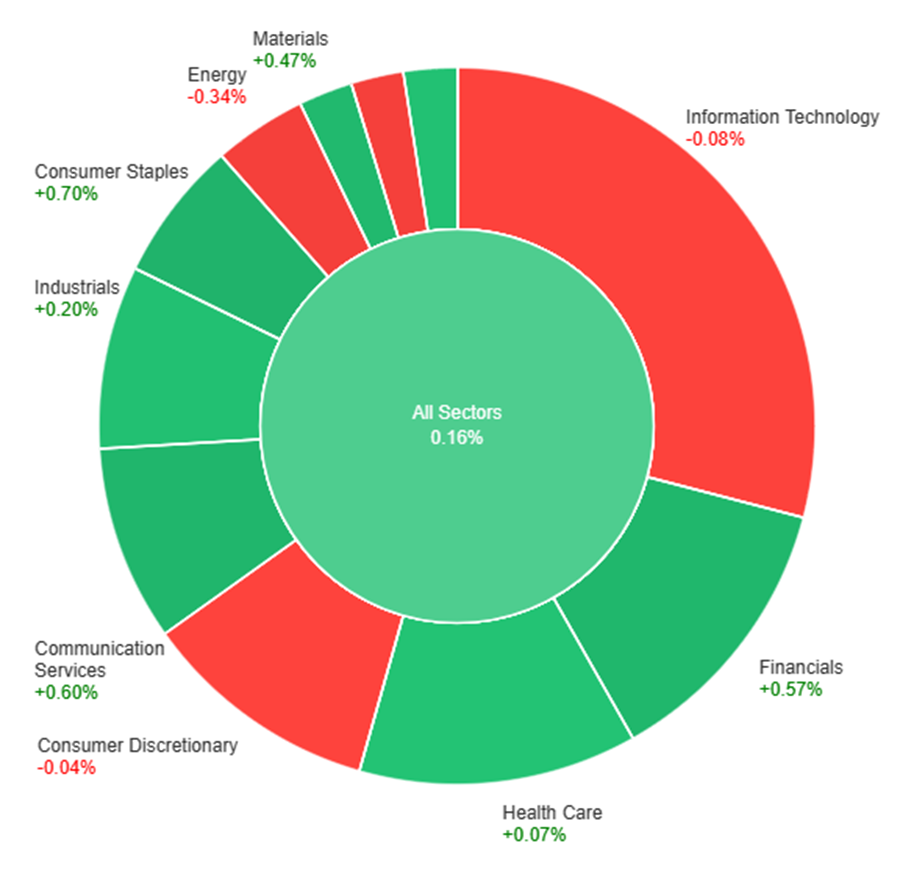

On Wednesday, the market showed a mix of positive and negative movements across sectors. Sectors like Consumer Staples (+0.70%), Communication Services (+0.60%), and Financials (+0.57%) saw gains, while Information Technology (-0.08%), Utilities (-0.33%), and Energy (-0.34%) experienced slight declines. Overall, the market displayed a balanced but somewhat subdued performance with some sectors in the positive territory and others marginally down.

Currency Market Updates

Recent currency market fluctuations, especially regarding the US dollar, reflect a responsive pattern to economic data and evolving rate forecasts. Following Tuesday’s post-CPI decline, the US dollar index saw a rebound fueled by stronger-than-expected US retail sales. This upward momentum in sales contributed to a rise in US Treasury yields, which helped alleviate the intensified selling pressure on the US currency. As a result, the extreme dovish predictions for Federal Reserve rate cuts in the second quarter of 2024 and beyond were tempered, with the market recalibrating its year-end rate-cut estimates.

The EUR/USD pair encountered a 0.3% drop to 1.0848 amidst the surge in US Treasury yields, unable to breach the resistance level of around 1.0882 for the second consecutive session. In contrast, USD/JPY surged past the 151 mark, targeting the 2022 high at 151.94, buoyed by favorable US-Japan rate spreads and the absence of pronounced dovishness from the Fed or hawkishness from the BoJ. Conversely, GBP/USD faced downward pressure, initially triggered by lower-than-expected UK CPI figures and further exacerbated by the robust performance of US retail sales. Additionally, commodity-linked currencies like CAD and AUD maintained modest gains despite a decline in oil prices, leveraging the rise in global growth expectations prompted by falling rates and the US dollar’s resurgence.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Retracement Amidst Fed Sentiment: Analyzing Dollar Dynamics

The EUR/USD pair experienced a corrective dip from its recent highs near 1.0900 to around 1.0830. Nevertheless, the prevailing bias suggests an upward trajectory, driven by declining confidence in the US Dollar. The Federal Reserve’s apparent conclusion on interest rate hikes following subdued inflation data triggered a Dollar retreat. However, the USD showcased resilience post-data release, backed by a rebound in US yields. While the negative Dollar sentiment prevails, the USD’s strength is evident against a backdrop of comparatively robust US economic performance. This correction in EUR/USD is viewed as a temporary adjustment in light of ongoing market expectations regarding the Fed’s stance on rates. The coming US economic data could further impact the pair’s movement.

Technical analysis shows a slight downward movement in the EUR/USD on Wednesday as it eased from the upper band of the Bollinger Bands. Presently, the pair is trading between the middle and upper bands, hinting at a potential slight decline towards the middle band. Additionally, the Relative Strength Index (RSI) stands at 71, indicating a sustained bullish bias.

Resistance: 1.0890, 1.0935

Support: 1.0835, 1.0772

XAU/USD (4 Hours)

XAU/USD Edges Lower Amid Dollar Rebound: Short-Term Upside Bias Persists

Spot Gold, represented by XAU/USD, encountered a retreat after hitting a weekly peak at $1,975, struggling to maintain ground above $1,970. This pullback was influenced by a US Dollar correction and a resurgence in US yields. Despite this, the immediate trajectory for Gold seems inclined toward further upward movement. Recent economic data, including the Producer Price Index (PPI), decline and softer Retail Sales, suggests a cooling of inflationary pressures, reinforcing the Dollar’s dip on Tuesday. Factors such as ongoing risk appetite, sturdy US bonds, and the Dollar’s vulnerability may continue to bolster Gold’s prospects. However, upcoming US releases like the Jobless Claims report and Industrial Production could potentially sway market sentiments, impacting Gold’s trajectory amid changing yield dynamics.

Technical analysis indicates that XAU/USD remained stable on Wednesday, aiming for the middle band of the Bollinger Bands. Currently, the gold price hovers slightly above this band, hinting at a potential minor decline towards this level. The Relative Strength Index (RSI) is currently at 52, indicating that the XAU/USD pair is still exhibiting a neutral bias.

Resistance: $1,970, $1,992

Support: $1,955, $1,933

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

USD

Unemployment Claims

21:30

221K

Written on November 16, 2023 at 2:21 am, by anakin

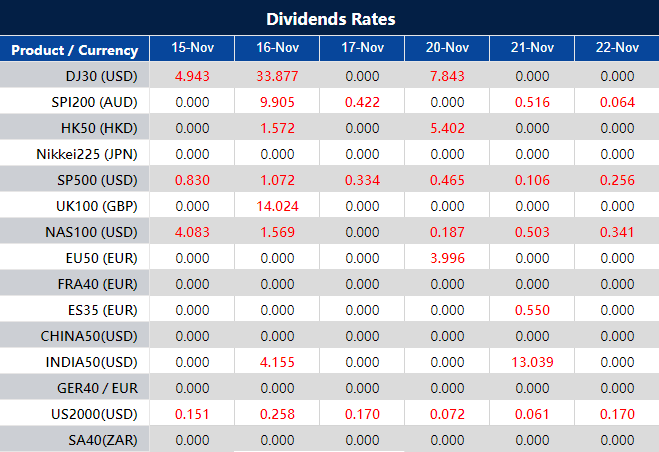

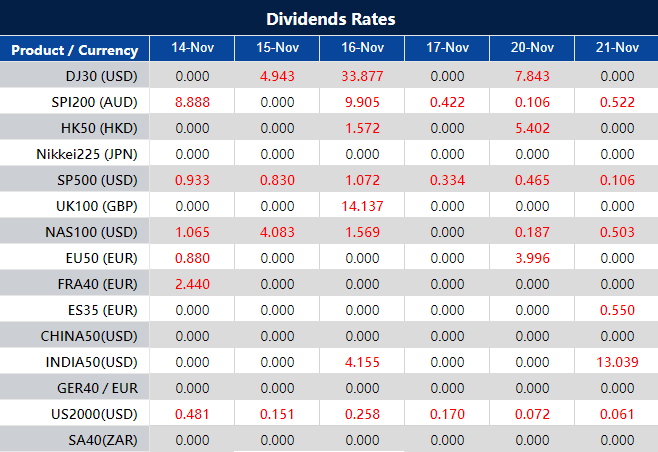

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Written on November 15, 2023 at 7:35 am, by anakin

The stock market witnessed a robust surge buoyed by an optimistic response to the latest US inflation report. Major indices like the Dow Jones, S&P 500, and Nasdaq rallied significantly, with tech stocks, in particular, hitting record highs. The lower-than-expected CPI figures fueled hopes of a sooner-than-anticipated end to the Federal Reserve’s rate hikes, leading to drops in the dollar and favorable movements in various asset classes, including stocks and precious metals. The market’s reaction also triggered shifts in rate expectations, influencing currency pairs like EUR/USD, USD/JPY, and GBP/USD, while highlighting divergent rate trajectories between different central banks by December 2024.

Stock Market Updates

The stock market experienced a robust rally fueled by optimistic sentiments following a favorable U.S. inflation report. The Dow Jones Industrial Average surged by 489.83 points, marking a 1.43% increase, while the S&P 500 rallied by 1.91%, briefly crossing the significant 4,500 threshold. This surge, the most substantial since April for the broad-market index, was met with the Nasdaq Composite jumping by 2.37% to close at 14,094.38. These gains contributed to an already impressive month for stocks, with the S&P 500 and Dow marking increases of 7.2% and 5.4%, respectively, in November, while the Nasdaq soared by 9.7%, on track for its most significant monthly gain since January.

The market’s upbeat response was primarily driven by the latest Consumer Price Index (CPI) figures, which indicated a stagnant inflation rate, contrary to expectations of a slight increase. This lower-than-anticipated core CPI, stripping out food and energy prices, presented the slowest rise in two years. This development buoyed hopes that the Federal Reserve might conclude its rate-hiking campaign sooner than anticipated. As a result, fed-funds futures pricing suggested a likelihood of steady rates at the next Fed policy meeting, fostering a market environment that saw the 10-year Treasury yield drop below 4.5%. Technology stocks surged notably, with the Technology Select Sector SPDR Fund hitting a record high, and specific companies like Tesla experiencing gains of more than 6%. Additionally, sectors sensitive to rate hikes, like banks, including Bank of America and Wells Fargo, witnessed substantial jumps amid hopes that the economy could avoid a recession. Among individual stock performances, Home Depot’s impressive 5% surge based on better-than-expected third-quarter earnings led the Dow’s gains, while companies like Enphase Energy, Boston Properties, and SolarEdge Technologies each climbed over 10%, contributing to the S&P’s upward trajectory.

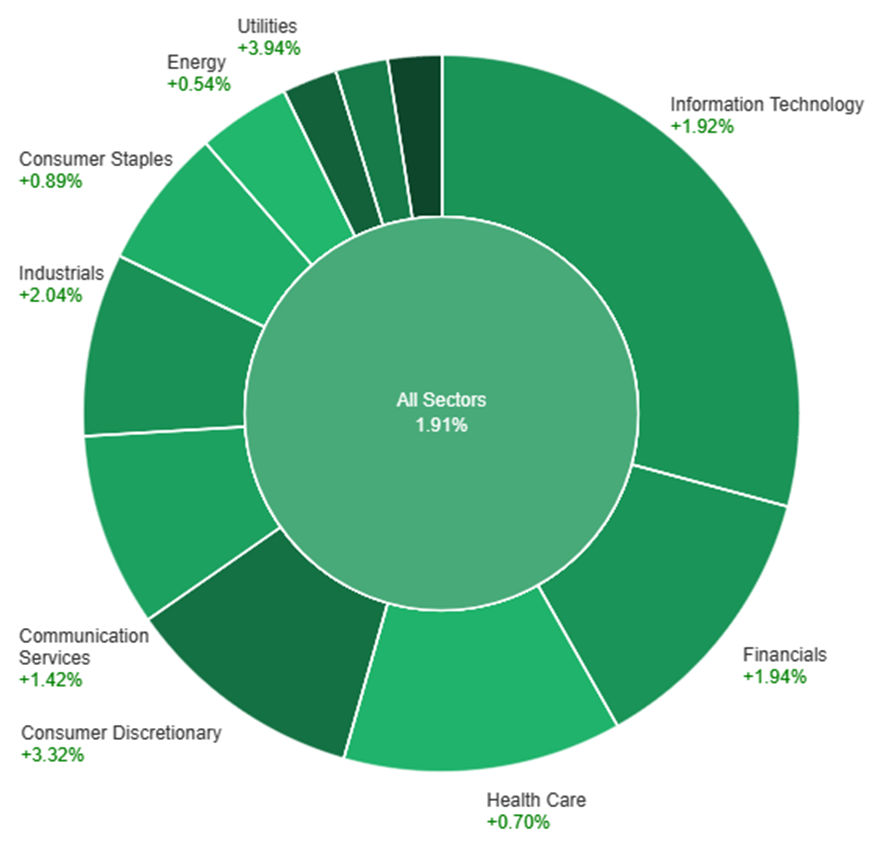

On Tuesday, the overall market saw a strong upswing with a notable gain of 1.91%. Real Estate emerged as the top-performing sector, soaring at 5.32%, followed by the Utilities and Consumer Discretionary sectors, which rose by 3.94% and 3.32%, respectively. Materials and Industrials also showed significant increases of 2.91% and 2.04%. Meanwhile, Financials and Information Technology experienced moderate gains of 1.94% and 1.92%. Communication Services followed suit with a rise of 1.42%, while Consumer Staples and Health Care showed more modest increases of 0.89% and 0.70%. Energy had the smallest increase at 0.54%, rounding up the day’s performance across sectors.

Currency Market Updates

The US dollar suffered a significant decline following the release of below-expected US CPI data, erasing lingering concerns of a hawkish Fed stance. The soft inflation figures prompted investors to recalibrate their projections for Fed rate cuts, moving the expected timeline to begin around May-June 2024 instead of June-July. Market sentiment now anticipates a substantial 98 basis points of Fed easing by December 2024, a stark shift from the earlier projection of -73 basis points prior to the data release. This adjustment in rate expectations heavily impacted the US yield curve, notably causing drops of 20 basis points in 2-7-year Treasury yields and 17 basis points in 10-year yields. The market reaction favored risk assets, with the S&P 500 surging by 1.9%, gold climbing 0.85% to $1,962, and silver rising by 3.4%.

The fluctuating dollar also influenced major currency pairs, with the EUR/USD gaining 1.6% as the Fed’s rate outlook aligned more closely with the ECB’s lower rate expectations. Conversely, the USD/JPY fell 0.75% as decreased Fed rate projections alleviated pressure from the US-Japan rate spread, impacting the pair’s positioning near its 2022 high. GBP/USD saw a rise of 1.76% to 1.2492, benefitting from compressed rate spreads. Sterling’s upward momentum above key resistance levels signals potential further gains, particularly as attention shifts to the UK CPI data for insights into the Bank of England’s potential actions amid the post-pandemic recovery. Meanwhile, the Australian dollar outpaced the Canadian dollar, bolstered by the RBA’s recent rate hike, while futures markets indicate a divergence in expected rate trajectories between the BoC and the Fed by December 2024.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Surges on Dollar Weakness Triggered by US CPI Data

The EUR/USD pair saw a substantial 200-pip surge following a Dollar selloff catalyzed by the release of stagnant US consumer inflation data. Despite the Eurozone experiencing a slight contraction, the Dollar’s tumble to monthly lows came as US CPI remained unchanged in October, sparking Treasury bond rallies and Wall Street stock gains. This shift strengthened the Euro against the Dollar, with expectations firming that the Federal Reserve might hold off on further rate hikes. The upcoming US Producer Price Index (PPI) release and October Retail Sales report are anticipated to provide further insights, potentially keeping the US Dollar vulnerable pending signs of easing inflation and consumer softness.

According to technical analysis, the EUR/USD moved higher on Tuesday, reaching above the upper band of the Bollinger Bands. Currently, the EUR/USD is trading just above the upper band, indicating the potential for a continuation move to widen the band further. The Relative Strength Index (RSI) is at 79, signaling a bullish bias for the EUR/USD.

Resistance: 1.0890, 1.0935

Support: 1.0835, 1.0772

XAU/USD (4 Hours)

XAU/USD Surges Amidst Dollar Decline and Inflation Data: Market Anticipates Fed’s Move

Spot Gold experienced a significant surge, propelled by a notable downturn in the US Dollar and an upswing in Treasury bonds. Climbing from $1,945 to $1,970, its highest in six days, XAU/USD rallied following the release of US inflation figures that triggered a strong market response, bolstering stocks and pushing the Dollar to multi-month lows. The Consumer Price Index showed a drop in annual inflation rates, below market expectations, easing speculation of a Federal Reserve rate hike before year-end. This led to a shift in market sentiment, advancing predictions for an earlier rate cut. With upcoming data releases on the Producer Price Index and Retail Sales, further evidence of softening inflation and consumer metrics might sustain Gold’s rally, reinforcing beliefs that the Fed’s tightening phase has reached its conclusion.

According to technical analysis, XAU/USD moved higher on Tuesday and managed to reach the upper band of the Bollinger Bands. Presently, the price of gold is moving just below the upper band, creating the possibility of further upward movement to push towards the upper band. The Relative Strength Index (RSI) is currently at 56, indicating that the XAU/USD pair is still in a neutral bias.

Resistance: $1,970, $1,992

Support: $1,955, $1,933

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

GBP

CPI y/y

15:00

4.7%

USD

Core PPI m/m

21:30

0.3%

USD

PPI m/m

21:30

0.1%

USD

Core Retail Sales m/m

21:30

– 0.1%

USD

Retail Sales m/m

21:30

– 0.3%

USD

Empire State Manufacturing Index

21:30

– 3.3

Written on November 15, 2023 at 1:49 am, by anakin

In order to provide you with a better user experience, VT Markets will upgrade our MT4 software to version 1380 on November 18, 2023 (Saturday). During this upgrade period, the MT4 trading software will be temporarily unavailable for login and use. However, this will not impact your existing trading orders, and there will be no changes to your trading account or login password for the software.

If your current software version has not been updated, we sincerely recommend that you synchronize and upgrade to the latest version 1380 after November 18, 2023.

Check your MT4 software version with the following steps:

※ PC: Open the MT4 software>Help>About;

※ Android: Open the MT4 app>About;

※ iOS: Open the MT4 app>Settings>Settings.

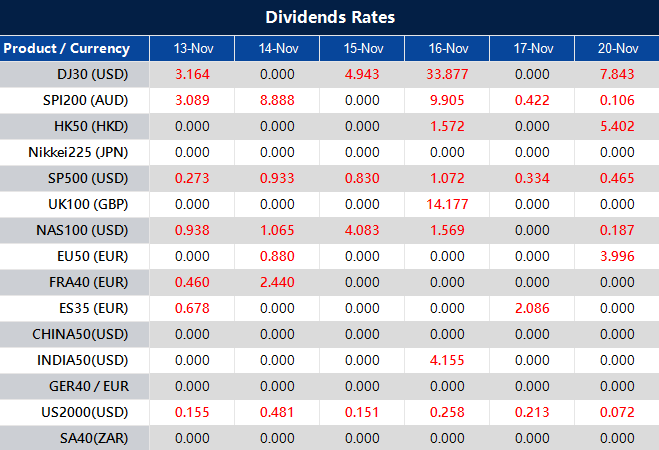

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Written on November 14, 2023 at 7:44 am, by anakin

In Monday’s trading session, the S&P 500 closed with minimal change, while the Nasdaq and Dow Jones showed varied movements. Investors awaited October’s Consumer Price Index (CPI) data, predicting a 3.3% year-over-year growth in inflation. Moody’s highlighted the U.S. fiscal deficits and political gridlock but maintained its AAA credit rating. The dollar retreated slightly as traders anticipated the CPI release, impacting currency markets. The EUR/USD pair gained, reflecting a dovish market sentiment. In other currencies, USD/JPY remained near flat, and GBP/USD rose due to political developments and hawkish Bank of England comments. Treasury yields saw a slight increase, gold rose, and silver edged up, aligning with expectations of a steady Federal Reserve. Bitcoin fell influenced by a cautious Fed rate outlook but remained near trend highs.

Stock Market Updates

On Monday, the S&P 500 closed nearly unchanged, down 0.08% at 4,411.55, and the Nasdaq Composite dipped 0.22% to close at 13,767.74. In contrast, the Dow Jones Industrial Average advanced 0.16%, gaining 54.77 points and closing at 34,337.87. Traders were cautiously awaiting the release of October’s consumer price index (CPI) data, a key indicator of inflation. Economists predicted a 3.3% year-over-year growth in headline inflation, with a 0.1% increase from the previous month. The market sentiment appeared cautious as investors monitored economic indicators for potential impacts on future Federal Reserve policies.

Additionally, Moody’s highlighted the United States’ “very large” fiscal deficits and political gridlock as factors influencing a negative outlook. Despite this, Moody’s reaffirmed the country’s credit rating at AAA, the highest level. This assessment followed Fitch’s downgrade of the U.S. long-term foreign currency issuer default rating to AA+ from AAA three months earlier, citing anticipated fiscal deterioration, a growing debt burden, and political disagreements on fiscal matters. Despite these concerns, Treasury yields remained flat on Monday, with the 10-year Treasury note yielding 4.638%, up about 1 basis point, indicating a somewhat stable market response to the negative fiscal outlook.

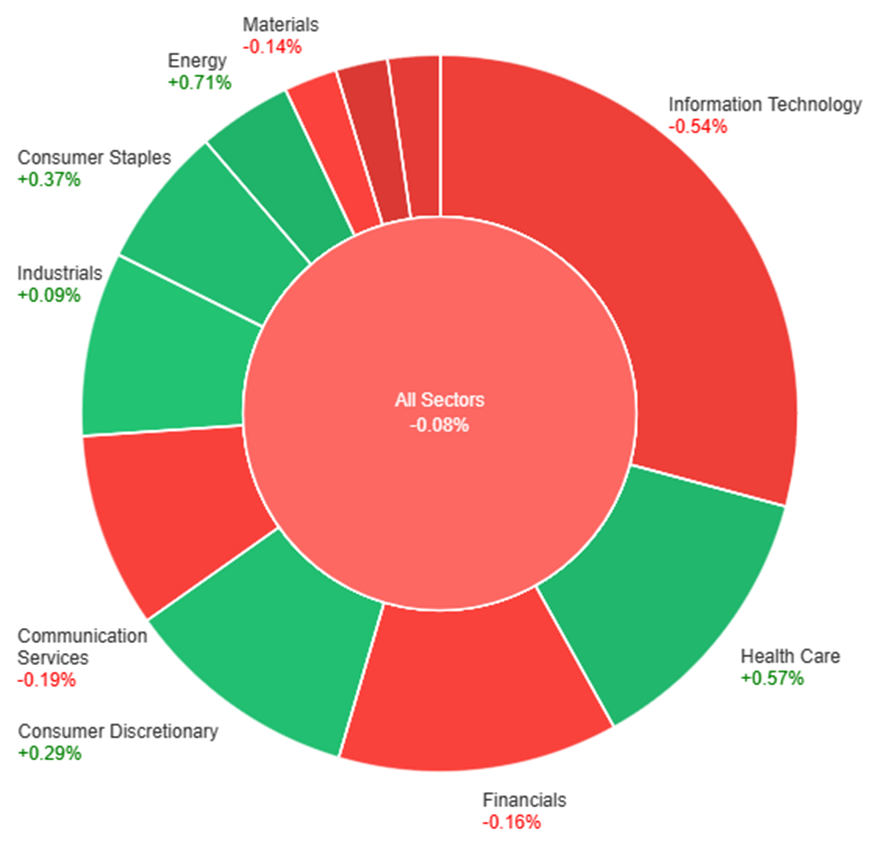

On Monday, the overall market experienced a slight decline of 0.08%. Among the sectors, Energy demonstrated the strongest performance with a gain of 0.71%, followed by Health Care at 0.57% and Consumer Staples at 0.37%. Consumer Discretionary and Industrials saw modest increases of 0.29% and 0.09%, respectively. In contrast, Materials, Financials, Communication Services, Information Technology, Real Estate, and Utilities all registered losses, with Utilities experiencing the most significant decline at 1.24%. The Information Technology sector led the declines with a decrease of 0.54%, contributing to the overall dip in the market on Monday.

Currency Market Updates

In the currency markets, the U.S. dollar experienced a mild retreat, holding slightly lower in U.S. afternoon trade despite earlier gains. Traders were in a state of anticipation as they awaited the release of the key U.S. Consumer Price Index (CPI) data scheduled for Tuesday. According to Reuters consensus forecasts, the core year-on-year inflation rate is expected to remain steady at 4.1%, while headline inflation is projected to decrease from 3.7% to 3.3%, influenced by a decline in oil prices. Although the anticipated core price stability is not anticipated to significantly impact Federal Reserve rate expectations, with futures markets indicating a pause in rate hikes and potential cuts in H2 2024, the market sentiment appeared more dovish ahead of the CPI release. The euro to U.S. dollar (EUR/USD) pair rallied 0.14%, asserting its influence on the U.S. dollar index as traders positioned themselves cautiously in anticipation of the CPI data, which seemed to have a more dovish impact than last week’s comments from Fed Chair Jerome Powell advocating for maintaining tight monetary policy to bring U.S. inflation back to the 2% target.

In other currency movements, the U.S. dollar to Japanese yen (USD/JPY) pair remained near flat after reaching a new high for 2023 at 151.92. However, it retreated from this peak due to reports of option-related activity, with approximately $3.45 billion set to mature during the week. Meanwhile, the British pound to U.S. dollar (GBP/USD) pair rose by 0.4% to 1.2276, driven by political developments in the UK that saw former Prime Minister David Cameron joining the Sunak government as foreign minister. Additionally, hawkish comments from Bank of England’s Catherine Mann, one of three Monetary Policy Committee members voting for a rate hike this month, contributed to the pound’s gains. Looking ahead, sterling traders are closely watching key events, including Tuesday’s UK employment and wage data and Wednesday’s UK CPI. Overall, Treasury yields saw a slight increase, gold rose by 0.5% to $1,946, and silver edged up 0.15% to $22.25, reflecting market expectations of a steady Federal Reserve and potential lower rates in 2024. Conversely, Bitcoin fell 1% to $36.7k, influenced by a more cautious Fed rate outlook, although it remained near trend highs supported by optimism surrounding crypto ETF registrations.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Gains Ground Amid Weaker Dollar and Eager Anticipation of Economic Data

The EUR/USD experienced a rise, finding support around 1.0560, propelled by a weakened US Dollar and declining US yields. This shift was influenced by a decrease in risk aversion, with Wall Street’s equity prices and commodity prices both on the upswing. As market attention turns to impending economic data releases from the US and Euro area, the focus centers on the US Consumer Price Index (CPI) report, with potential implications for interest rate decisions. A positive inflation outcome could strengthen the US Dollar, while a softer reading may boost the EUR/USD pair. Concurrently, Eurostat’s release of employment and growth data, with an expected 0.1% contraction, adds further anticipation, making the upcoming period crucial for EUR/USD dynamics.

According to technical analysis, the EUR/USD moved slightly higher on Monday, reaching above the middle band of the Bollinger Bands. Currently, the EUR/USD is trading just above the middle band, indicating the potential for a consolidating move to try to reach the upper band. The Relative Strength Index (RSI) is at 56, signaling that the EUR/USD is back in a neutral bias.

Resistance: 1.0725, 1.0755

Support: 1.0679, 1.0645

XAU/USD (4 Hours)

XAU/USD Slide to Near-Month Low as Safe-Haven Appeal Wanes Amid Hawkish Global Policies

XAU/USD continues its decline, reaching $1,918.35, its lowest point in nearly a month. Despite a less optimistic market sentiment, safe-haven assets, particularly Gold, remain unattractive, contributing to the precious metal’s downward trend. Global policymakers maintain a hawkish stance, dispelling speculation of an end to the tightening cycle or potential rate cuts in 2024. Concerns persist about inflationary pressures, as central banks hesitate to raise rates consistently, and tight labor markets hinder economic slowdown. Investors await the release of October inflation figures from the United States on Tuesday for potential insights into future market dynamics.

According to technical analysis, XAU/USD moved slightly higher on Monday and managed to reach the middle band of the Bollinger Bands. Presently, the price of gold is moving just below the middle band, creating the possibility of moving slightly higher above the middle band. The Relative Strength Index (RSI) is currently at 45, indicating that the XAU/USD pair is back in a neutral bias.

Resistance: $1,962, $1,992

Support: $1,945, $1,920

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

GBP

Claimant Count Change

15:00

15.0K

USD

Core CPI m/m

21:30

0.3%

USD

CPI m/m

21:30

0.1%

USD

CPI y/y

21:30

3.3%

Written on November 14, 2023 at 1:00 am, by anakin

This week is anticipated to be one of heightened activity for market participants, with a particular focus on developments within the United States. Noteworthy economic indicators, specifically the Consumer Price Index (CPI), Producer Price Index (PPI), and Retail Sales data, are scheduled for release. These reports are expected to introduce substantial volatility and potentially set the directional course for the US Dollar.

It’s crucial for traders to be cautious and stay on top of the latest developments for a successful week of trading.

UK Claimant Count Change (14 November 2023)

The Claimant Count Change in the UK rose to 20,400 in September 2023, up from -9,000 in August 2023.

The next figures will be released on 14 November, with analysts anticipating an increase of 25,000.

US Consumer Price Index (14 November 2023)

Consumer prices in the US increased by 0.4% month-on-month in September 2023, easing from a 0.6% rise recorded in August.

Analysts expect a 0.1% increase in the figures for October, which are due for release on 14 November.

Australia Wage Price Index (15 November 2023)

Australia’s seasonally adjusted wage price index rose by 3.6% year-on-year in Q2 2023, slightly down from the 3.7% increase seen in Q1 2023.

The data for Q3 2023 is set to be released on 15 November, with analysts expecting an uptick to 3.8%.

UK Consumer Price Index (15 November 2023)

The UK’s inflation rate remained steady at 6.7% in September 2023, consistent with the 18-month low observed in August.

The upcoming CPI figures are projected to indicate a further decrease to 4.9%.

US Producer Price Index (15 November 2023)

Producer prices in the US increased by 0.5% month-over-month in September 2023, the smallest rise in three months after a 0.7% increase in August.

The data for October 2023 will be released on 15 November, with analysts forecasting a modest 0.1% increase.

US Retail Sales (15 November 2023)

Retail sales in the US increased by 0.7% month-on-month in September 2023, following an increase of 0.8% in August.

Analysts expect a slight decrease of 0.1% in the October figures, which are scheduled for release on 15 November.

Employment in Australia (16 November 2023)

Employment in Australia grew by 6,700 in September 2023. Meanwhile, the unemployment rate unexpectedly fell to a three-month low of 3.6% in the same peried, a marginal decrease from the figure recorded in August.

Analysts expect the employment figures for October 2023 to reveal an increase of 24,900, with the unemployment rate predicted to remain steady at 3.6%. The data are scheduled to be released on 16 November.

UK Retail Sales (17 November 2023)

Retail sales in the UK declined by 0.9% month-over-month in September 2023, reversing a 0.4% increase in August.

Analysts anticipate that UK retail sales for October 2023, which are to be released on 17 November, will increase by 0.3%.

Written on November 14, 2023 at 12:36 am, by anakin

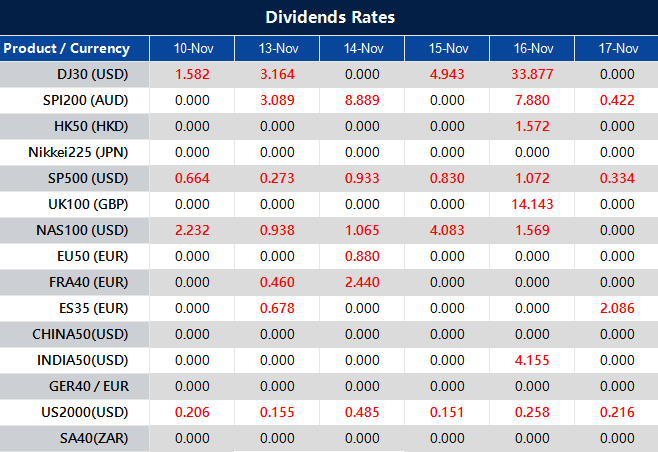

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Written on November 13, 2023 at 7:02 am, by anakin

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Written on November 10, 2023 at 8:15 am, by anakin