VT Markets brought the excitement off the pitch and into the fans’ hands at the recent South Korea clash between Newcastle United and Tottenham Hotspur. As proud sponsors of the Fanzone and Hyundai Mall pop-up, we created immersive experiences that connected supporters with the game beyond the stadium – celebrating our partnership with NUFC and engaging fans in unforgettable ways.

VT Markets and Newcastle United Kick Off Global Partnership

VT Markets and Newcastle United officially launched their global partnership at the J. League International Series in Japan, held at the Saitama Stadium. The event featured the unveiling of a special ‘77’ jersey, symbolizing good fortune and growth for VT Markets. In a gesture of appreciation, Newcastle United presented the curated jersey, while VT Markets reciprocated with a trophy. Key figures, including Agustin Bilinskis, Head of Strategy Operations, APAC, and Dandelyn Koh, Global Brand Lead for VT Markets, alongside Newcastle United’s Peter Silverstone, marked the beginning of this exciting collaboration aimed at mutual success.

Festival of Football 2025

This July, join us in Singapore for an exciting 4-day curated experience that combines world-class football action with elevated hospitality and curated city exploration.

Enjoy premium access to a high-energy match on 27 July at the National Stadium, where Arsenal returns to face newly-crowned Carabao Cup champions Newcastle United, who are playing in Singapore for the first time since 1996.

Designed to celebrate our most valued clients, this experience goes beyond the game—featuring not just elite matchday access, but also opportunities to explore Singapore’s vibrant culture, network with fellow guests, and enjoy the outstanding service VT Markets is proud to provide.

Nikkei 225 slips as traders cash in gains

Japanese equities are pausing after a strong rally, with investors turning cautious ahead of central bank signals and geopolitical developments that could set the tone for market moves.

Investor caution weighs on Tokyo markets

The Nikkei 225 retreated on Tuesday after recently setting fresh record highs, as investors shifted to profit-taking ahead of major economic and geopolitical developments. The broader Topix index also edged lower by 0.1% to 3,118, reflecting a more cautious market mood.

Attention remains on US President Donald Trump’s calls for Russia-Ukraine peace talks, urging President Putin to prepare for a potential summit with Volodymyr Zelenskiy.

At the same time, traders are awaiting Federal Reserve Chair Jerome Powell’s speech at the Jackson Hole symposium later this week, hoping for clarity on the Fed’s policy outlook after a run of mixed inflation and labour market data.

In corporate moves, SoftBank slipped 2% after reports suggested it is considering a $2 billion investment in US chipmaker Intel.

Other notable decliners included Sanrio (-6.5%), Fujikura (-3.2%), and Mitsubishi UFJ (-2%), all of which added to the downward pressure on sentiment.

Technical analysis

The Nikkei 225 has extended its strong rebound from the April low of 30,397, climbing as high as 43,606 before pausing.

The long-term outlook remains bullish, with prices trading well above both short- and medium-term moving averages, underlining continued buying momentum.

Picture: Nikkei 225 trades near 43,606, showing a gradual recovery from April lows with momentum supported above key moving averages, shown on the VT Markets app.

The MACD indicator stays in positive territory, signalling underlying strength, though the flattening histogram suggests that upward momentum may be slowing in the near term.

Immediate resistance is seen at 43,600–43,800, an area where recent highs have capped gains. A decisive break above this range could open the way to 44,500.

On the downside, initial support stands at 42,500, followed by stronger levels around 39,800. As long as the index holds above its rising 30-day moving average, the broader bullish structure remains intact, though short-term pullbacks remain likely after the extended rally.

Cautious forecast

Looking ahead, the market’s direction will largely depend on central bank messaging and geopolitical progress.

Should Powell deliver a dovish tone at Jackson Hole, Japanese equities could quickly regain momentum, with the Nikkei retesting recent highs and potentially breaking back above 44,000.

A softer policy stance would reassure investors that the Fed remains supportive of economic growth, bolstering risk sentiment in global equities.

On the other hand, a hawkish message that prioritises inflation control could dampen appetite for risk assets, prompting further profit-taking.

In addition, uncertainty surrounding Russia-Ukraine talks poses another layer of potential volatility, with investors closely watching whether negotiations materialise or stall.

In such a scenario, the Nikkei could extend its correction, with downside risks initially at 42,500 and, if sentiment weakens further, around 41,500.

Overall, while the broader trend remains constructive, traders may prefer a cautious, flexible approach as global developments continue to shape the outlook.

Click here to open account and start trading.

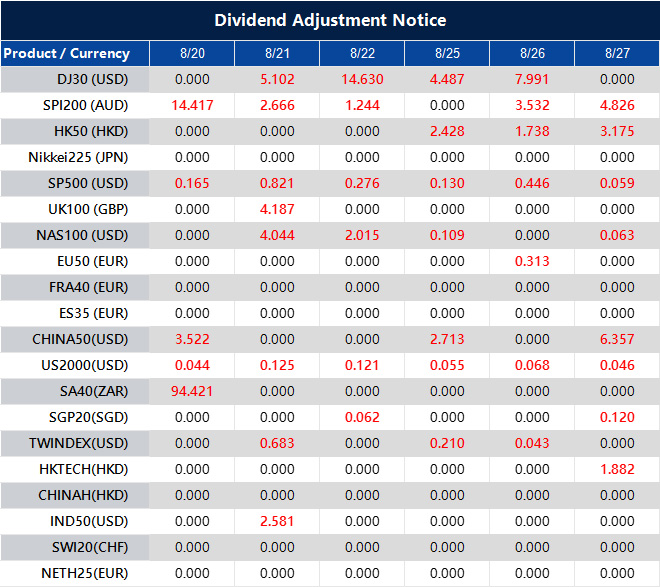

Dividend Adjustment Notice – Aug 20 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

An Exclusive Matchday Experience, Crafted by VT Markets – NUFC vs Everton

Join VT Markets for an exclusive 6-day football journey across the UK from May 22–27, 2025.

Begin in London with a welcome dinner and city tour, then travel to Newcastle for an exclusive experience with our partners, Newcastle United. Enjoy a training ground visit, a possible stadium tour, and the main highlight—matchday at St. James’ Park as NUFC takes on Everton, followed by a post-match party.

Wrap up with a media event and meet-and-greet, leaving with unforgettable memories of Premier League action and VT Markets hospitality.

Crypto rally cools as Bitcoin and Ethereum consolidate

The crypto market is cooling after its recent rally, with Bitcoin and Ethereum losing some momentum. This shift signals a pause rather than an end to the trend, putting the focus on risk management and smarter positioning over chasing quick gains.

Bitcoin and Ethereum face momentum shift

Bitcoin (BTC) and Ethereum (ETH) are retreating after recent gains, with BTC down around 2% and ETH sliding more than 3% at the time of writing.

This pullback follows a strong rally in previous weeks, suggesting a notable shift in short-term market dynamics.

On broader timeframes, BTC has slipped below its 50-day moving average – a technical sign that the recent uptrend is losing steam.

The next major support zone for BTC sits near $112,000, marked by the 2 August low and the 22 May high.

Profit-taking has been a key driver of this correction, particularly among late entrants chasing record highs.

Risk management becomes a priority

As Bitcoin and Ethereum give back some of their recent advances, traders are shifting focus from chasing upside to protecting gains.

The drop under the 50-day moving average highlights the need for a more defensive stance. Buying protective put options has become a popular hedging strategy, with the Bitcoin put-to-call ratio climbing to 0.75 – its highest level in over a month.

This signals rising demand for downside protection as market participants prepare for the possibility of a deeper pullback towards the $112K support.

At the same time, Ethereum’s implied volatility has spiked, with 30-day at-the-money volatility in ETH options jumping from 50% to 65% in just a few days.

For traders expecting sharp moves but uncertain about direction, strategies like long straddles or strangles could capture potential gains, regardless of whether the next big move is upward or downward.

Opportunities amid consolidation

For traders who view this downturn as a healthy consolidation before another leg higher, selling cash-secured puts near the $112K support could offer an attractive entry point.

This approach allows them to collect option premiums while defining a preferred level to re-accumulate BTC, maintaining confidence in the long-term bullish structure.

The current setup also carries echoes of the summer 2021 cycle, where a sharp multi-week correction followed a strong rally before the market rallied again to new all-time highs.

With open interest levels holding relatively steady, it appears that large positions have not yet been fully unwound.

This suggests that while caution is warranted in the short term, the broader trend may still be intact – with this phase representing consolidation rather than the end of the cycle.

Click here to open account and start trading.

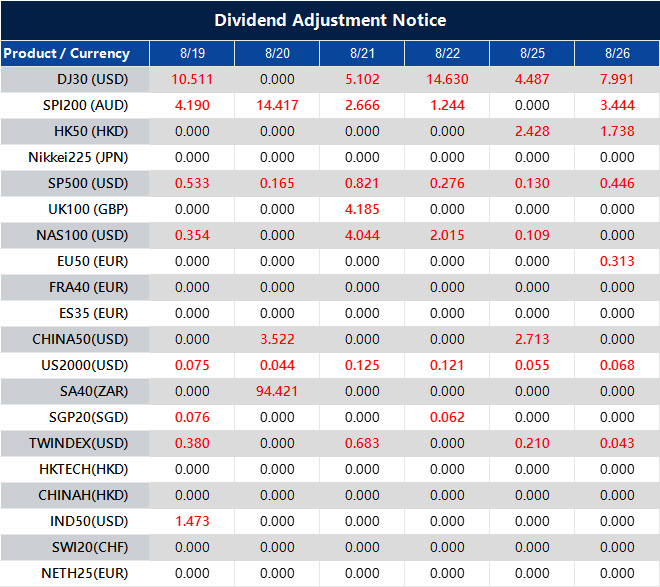

Dividend Adjustment Notice – Aug 19 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Pre-Market and After-Hours Trading: How to Trade Before and After the Bell

Trading doesn’t stop when the closing bell rings. With pre-market and after-hours trading, also known as extended hours trading, investors can buy and sell shares outside regular market hours. These extended hours trading sessions allow traders to react quickly to earnings reports, economic data, or global news that can move prices overnight. Understanding how they work, along with their benefits and risks, is key to using extended hours trading effectively.

What Is Pre-Market and After-Hours Trading?

Stock exchanges such as the New York Stock Exchange (NYSE) and NASDAQ operate on fixed schedules, but trading does not always end when the closing bell rings. Pre-market trading takes place before the exchange officially opens, while after-hours trading occurs after it closes. Together, these extended hours sessions allow traders to buy and sell outside the regular market, offering more flexibility to react to news and global events.

Pre-market trading usually runs from 4:00 a.m. to 9:30 a.m. Eastern Time in the U.S., while after-hours trading begins at 4:00 p.m. and typically lasts until 8:00 p.m. Eastern Time. Some brokers may limit access to 7:00 p.m. or extend trading beyond 8:00 p.m., depending on their policies. These sessions are part of extended hours trading, and their exact timing is determined by the stock exchange.

These trading windows are especially important for reacting to market-moving events. For example, Apple often releases its earnings reports after the NYSE closes, and its stock can swing sharply in after-hours trading before the next day’s opening session.

Discover the 10 largest stock exchanges in the world by market cap.

How Does Pre-Market and After-Hours Trading Work?

Pre-market and after-hours trading work through Electronic Communication Networks (ECNs), which match buyers and sellers directly without relying on a traditional exchange floor. Market makers, who provide liquidity during regular trading hours, are typically less active in after-hours trading, which contributes to wider bid-ask spreads. Because fewer participants are active during these times, liquidity is thinner, and spreads between bid and ask prices tend to be wider.

Most brokers only allow limit orders in extended hours. This means you must set a specific buy or sell price instead of relying on market orders. Accessing pre-market and after-hours trading typically requires a brokerage account that supports these sessions. This helps protect against sudden price swings but may result in orders not being filled if the price is not met.

Trading activity and trade volume are also much lower than in regular hours. For example, while millions of shares of Apple may trade during the main session, only a fraction of that volume is exchanged in pre-market or after-hours. This difference explains why small trades can cause larger price moves.

What Is Pre-Market Trading?

Pre-market trading, also known as trading during pre-market trading hours as defined by the stock exchange, takes place before the stock market officially opens. In the United States, pre-market hours usually run from 4:00 a.m. to 9:30 a.m. Eastern Time.

This trading session allows traders to respond to international market moves and overnight news. Liquidity is usually lower than in the main session, which means price changes can be more volatile. Large-cap companies such as Tesla, Amazon, and Microsoft often see the most activity in pre-market trading because they attract both institutional and retail interest. Pre-market is a distinct trading session with its own characteristics compared to regular and after-hours sessions.

What Is After-Hours Trading?

After-hours trading, also known as the after-hours session, begins once the official market closes and typically lasts from 4:00 p.m. to 8:00 p.m. Eastern Time in the U.S. This is one of the busiest periods for corporate announcements, as many companies release their earnings reports after the closing bell. Significant news or earnings releases during the after-hours session can have an immediate impact on a company’s stock price, as investors react to new information outside of regular trading hours.

For example, Amazon’s 2023 earnings release pushed its stock up more than 12 percent in after-hours trading, allowing active traders to trade after-hours and benefit before the next day’s open. However, these moves can also be sharp in the opposite direction if results disappoint.

Why Traders Use Pre-Market and After-Hours Trading

There are several reasons why traders look to pre-market and after-hours trading as part of their strategy:

1. Reacting quickly to news

Important announcements such as earnings reports, mergers, or unexpected economic data often occur outside of normal trading hours. Extended sessions allow traders to respond immediately instead of waiting until the next day.

2. Global alignment

International events in Asia or Europe frequently influence U.S. markets before the opening bell. Pre-market trading gives investors the chance to adjust positions based on overseas developments.

3. Capturing opportunities

Traders can establish positions before the main session begins, aiming to benefit from sharp moves that may continue into regular hours.

4. Flexibility for active investors

Extended hours provide more time windows to trade, which is particularly useful for those who cannot be active during standard market hours due to work or time zone differences.

Example: In April 2025, Meta Platforms’ stock jumped more than 11% in after-hours trading after reporting strong quarterly earnings and better-than-expected revenue driven by AI investments. Traders who acted quickly were able to capture gains before the market reopened the next day.

What Are the Risks and Challenges of After-Hours Trading?

While extended hours can create valuable opportunities, they also come with several risks that traders must carefully manage:

- Lower liquidity: Trading volume is much thinner compared to regular sessions. With fewer buyers and sellers, bid-ask spreads often widen, making it harder to get favorable prices. A trader might place an order at one price but only get filled at a much less attractive level. These liquidity challenges are especially pronounced outside regular trading hours and regular market hours.

- Higher volatility: With fewer participants in the market, even small orders can trigger outsized price swings. A stock that moves 1 percent during normal hours could easily shift 5 percent or more in after-hours trading, and price swings can be more pronounced in any given hour during extended sessions.

- Limited order types: Most brokers only allow limit orders during extended sessions. Market orders are generally restricted to protect traders from extreme price swings, but this also means execution may be delayed or partially filled. ECNs and other trading systems match buy and sell orders during these extended sessions, which can affect how and when trades are executed.

- Overreaction to news: Stocks often jump or fall sharply outside normal hours based on headlines or earnings results, only to reverse direction once the broader market opens and more participants enter.

- Less transparency: Not all price movements in extended hours reflect broader market sentiment. For example, a stock may appear to soar overnight, but the move could be based on very light volume that exaggerates the trend.

Example: In April 2025, Royal Caribbean shares initially rose 3% in reaction to strong earnings but then reversed course and fell 2.6% later in the session, illustrating how early enthusiasm in extended hours (e.g., after-hours trading) can quickly evaporate as more information and liquidity enter the broader market.

How to Trade Pre-Market and After-Hours

Trading outside regular hours requires preparation and awareness, as the process is slightly different from the main market session. To get started, follow these steps:

Step 1: Understand how pre-market and after-hours work

Know the trading hours, how liquidity differs from regular sessions, and the risks involved before you start.

Step 2: Select a reliable broker that offers extended hours

Not all brokers provide access to pre-market and after-hours trading. VT Markets gives traders nearly round-the-clock access to global markets and CFDs, offering flexibility to act on opportunities outside regular hours.

Step 3: Open and fund your trading account

Create an account with your chosen broker, then add funds to ensure you are ready to place trades during pre-market and after-hours sessions.

Step 4: Place your order

Most brokers only allow limit orders in extended hours trading to help you control execution prices.

Step 5: Implement risk management tools

Use tools like stop-loss orders, position sizing, and take-profit levels to manage risk effectively during volatile pre-market and after-hours trading.

Step 6: Stay updated and informed

Monitor earnings announcements, global news, and economic data releases that can impact stock prices outside regular hours.

Discover the best time to buy and sell stocks.

Common Mistakes to Avoid When Using Pre-Market and After-Hours Trading

Many new traders fall into avoidable errors when trading outside regular sessions. Here are six of the most common mistakes:

- Chasing sudden price spikes without checking volume: Price moves can look significant but may be misleading if they are based on very low trading volume. Always confirm liquidity before entering a trade to avoid chasing false signals.

- Using market orders in illiquid conditions: Bid-ask spreads widen outside regular hours, and market orders can execute at far worse prices than expected. Limit orders provide more control and help protect you from slippage.

- Taking oversized positions during volatility: Price swings are sharper in extended sessions, and large trades magnify both potential profits and losses. Keeping position sizes small helps manage risk.

- Ignoring potential reversals at the open: Moves that occur in pre-market or after-hours often fade once regular trading resumes and more participants join. Traders who ignore this risk can see overnight gains vanish quickly.

- Overreacting to initial news headlines: Earnings announcements or press releases can trigger dramatic moves, but details in the full report may shift market sentiment. Acting without deeper analysis can lead to poor entries.

- Failing to apply risk management strategies: Skipping stop-losses, ignoring take-profit levels, or neglecting position sizing exposes traders to heavy losses in highly volatile conditions. Disciplined risk management is critical in extended sessions.

In Summary

- Pre-market trading runs before the opening bell, giving traders a chance to act on overnight or international developments.

- After-hours trading takes place after the close and is often driven by earnings releases and breaking news.

- Together, they form pre-market and after-hours trading, also called extended hours trading.

- These extended hours trading sessions offer flexibility and early opportunities to react to market-moving events but also carry higher risks, such as volatility and lower liquidity.

Start Trading Today with VT Markets

VT Markets offers access to global markets, competitive spreads, and powerful platforms like MetaTrader 4 (MT4) and MetaTrader 5 (MT5). Traders can also explore a VT Markets demo account to practice in real market conditions without risking their real capital. Our Help Centre provides valuable resources and support to improve trading confidence.

Start trading today with VT Markets and take advantage of opportunities in pre-market and after-hours sessions.

Frequently Asked Questions (FAQs)

1. How do pre-market and after-hours trading work?

Pre-market and after-hours trading, also called extended hours trading, allows investors to buy and sell stocks outside the regular market session.

2. What time does pre-market trading start?

In the U.S., pre-trading hours usually begin at 4:00 a.m. Eastern Time and last until the market opens at 9:30 a.m.

3. What is after-hours trading and why is it important?

After-hours trading happens after the market closes, usually between 4:00 p.m. and 8:00 p.m. Eastern Time. It is important because many companies release earnings during this time, creating sharp price movements.

4. Can retail traders participate in pre-market and after-hours trading?

Yes, many brokers allow retail traders to access extended hours, though there may be restrictions.

5. Why are stocks more volatile after-hours?

Because fewer participants are trading, supply and demand imbalances can lead to larger price swings.

6. Can I trade all stocks in pre-market and after-hours sessions?

No. Not every stock is available during extended hours. Larger companies with higher liquidity, such as Apple or Tesla, are usually more active, while smaller-cap stocks may see little to no trading.

7. Do price gaps in extended hours affect the next day’s opening price?

Yes. Sharp moves after-hours can lead to opening gaps the next morning, although prices often adjust once regular session trading volume increases.

8. What type of orders should I use in pre-market or after-hours trading?

Most brokers only accept limit orders during extended hours to protect traders from unexpected price swings. Market orders are generally not allowed.

9. Is extended hours trading suitable for beginners?

While it offers opportunities, pre-market and after-hours trading are riskier due to volatility and low liquidity. Beginners may benefit from practicing first with a demo account before trading live.

10. How does news released outside market hours impact trading?

Earnings reports, press releases, or economic data released after-hours often drive sharp moves. Traders active during these times can react immediately instead of waiting until the next day.

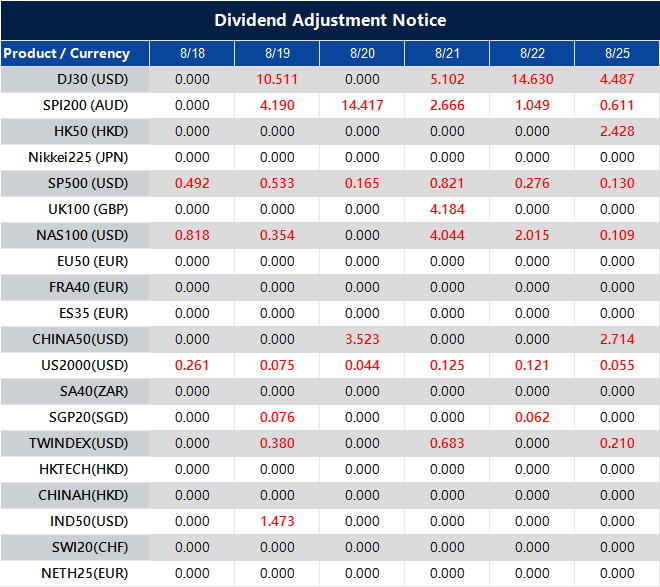

Dividend Adjustment Notice – Aug 18 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.