August 2025 has brought the latest US earnings season to a close, offering what is effectively a quarterly health check on corporate America. For traders, these updates are far more than company press releases – they are signals that drive price swings, shift sentiment, and open the door to opportunities.

A health check on corporate America

Earnings season refers to the stretch from mid-July to mid-August when listed companies disclose results from the April–June period. These updates cover profits, revenues, and forward guidance, giving markets a vital snapshot of business conditions.

They matter because they often set the tone: share prices can jump or fall sharply, while outlooks reveal how executives see the year ahead.

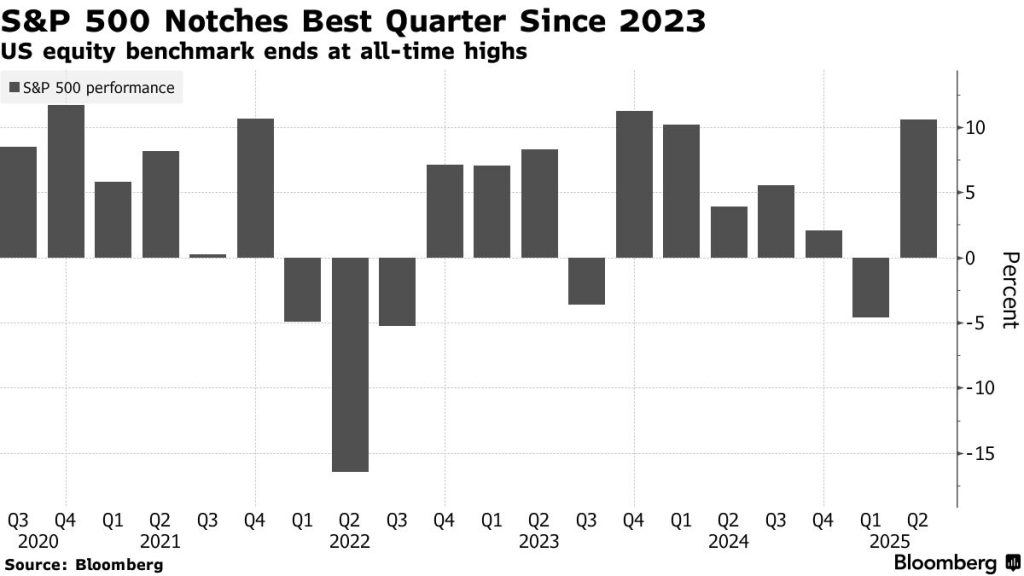

This time, the results were stronger than expected. S&P 500 companies collectively posted an 11.8% increase in earnings year-on-year, nearly double what analysts had predicted. Revenues rose by about 4–5%, and more than three-quarters of companies exceeded profit forecasts.

The season was not without volatility, though – the VIX, Wall Street’s “fear gauge”, swung up toward 20 as traders reacted to results in real time. For those active in shares or ETFs, Q2 showed that earnings remain the pulse of the market.

Strong results and market reactions

The headline story of Q2 was one of corporate resilience. Analysts had expected a modest 5–6% increase in earnings, but companies delivered nearly twice that.

Around 80% reported profits above forecasts, while top-line revenue growth held steady at 4–5%. Guidance for the rest of 2025 suggested businesses expect earnings to grow by roughly 9–10% for the year as a whole.

Markets responded positively. The S&P 500 rose about 2% across the reporting period, lifted by stronger-than-expected results in technology and consumer sectors.

Yet this optimism came with bursts of volatility. The VIX index jumped from the mid-teens to around 20 at points, underlining how quickly sentiment can swing when earnings hit the wires.

The mood among individual investors also shifted: the AAII survey showed bullish sentiment climbing above 55%, the highest reading in four years.

For traders, the message is twofold. Beating expectations still fuels rallies, but valuations remain stretched. With the S&P trading at roughly 22 times earnings – well above long-term averages – markets look increasingly sensitive to any disappointments.

The trends that shaped Q2

Behind the broad numbers, four clear trends emerged.

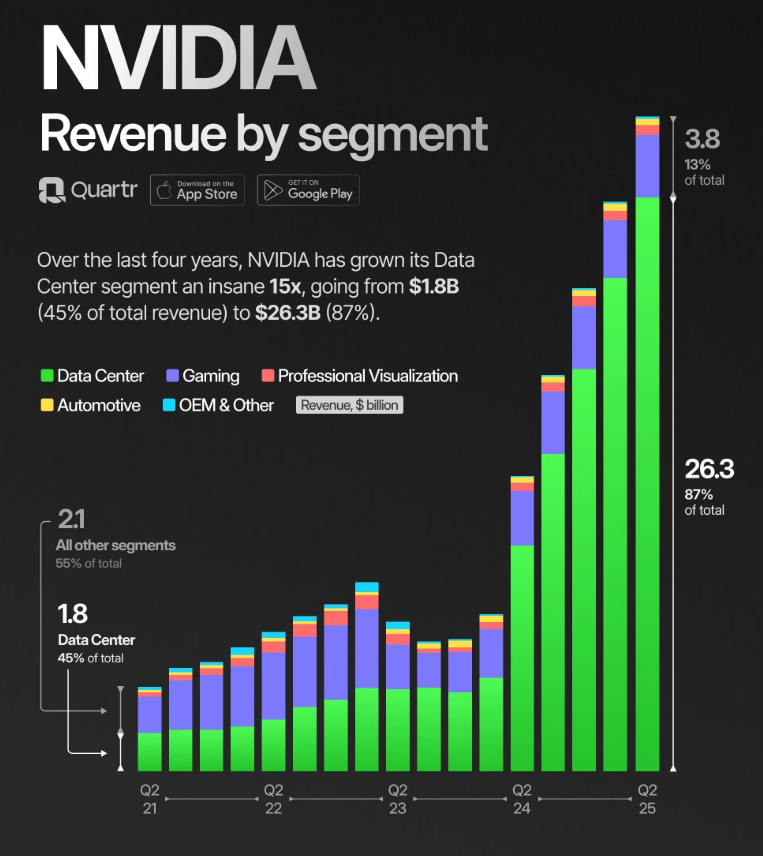

First, technology and artificial intelligence continued to dominate. Nvidia once again set the pace, reporting a staggering 122% jump in data centre revenue. Microsoft also impressed with 20% growth in its cloud division. These results underscored the central role AI now plays in market leadership. Tech is the engine of this market, and for now, it is still roaring.

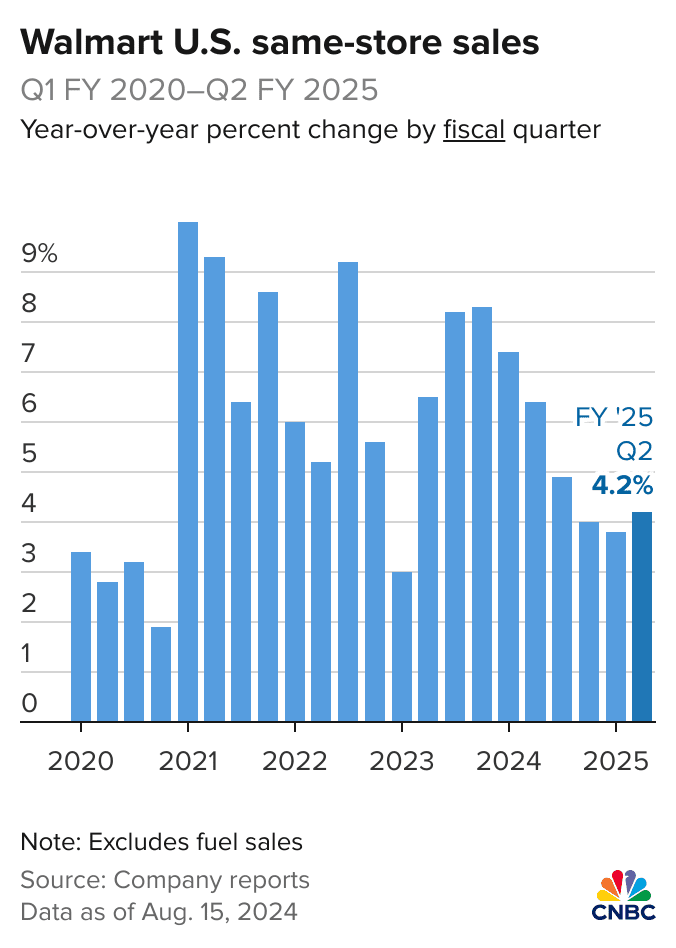

Second, the American consumer proved resilient. Retailers delivered upbeat results, with Walmart’s e-commerce sales climbing 25% and Target reporting solid gains as well. Banks reinforced the picture: JPMorgan noted steady loan growth and a 4% rise in payment volumes, suggesting that households are still spending despite high borrowing costs.

Third, investors showed signs of rotating towards defensive sectors. Utilities and consumer staples saw inflows as funds positioned against potential risks from new tariffs. While high-growth tech names stole headlines, the quieter move into defensives highlighted a measure of caution beneath the surface.

Finally, corporate guidance revealed a split in sentiment. Many companies pointed to robust demand, but industrials sounded the alarm over trade measures. Ford, for example, estimated an $800 million hit from new tariffs.

The balance between AI optimism and tariff anxiety captured the essence of this earnings season: a market buoyed by innovation but wary of political and macroeconomic headwinds.

How sectors performed

Sector performance in Q2 painted a mixed but instructive picture for traders.

Technology was the clear winner. Nvidia’s triple-digit growth and Microsoft’s cloud expansion drove the sector higher, with tech stocks broadly advancing by 5–10% through July. These remain the market’s momentum plays, though volatility makes timing critical.

Financials offered a steadier profile. JPMorgan’s results illustrated the sector’s resilience, with lending activity stable and consumer spending channels growing modestly. While not as headline-grabbing as tech, financials provided defensive balance in portfolios.

Consumer discretionary names told a more nuanced story. Retailers such as Walmart and Target outperformed expectations, proving the strength of everyday spending, but autos were hit hard. Ford’s tariff-related losses highlighted how vulnerable manufacturers remain to global trade disputes.

Elsewhere, healthcare and energy lagged behind, reflecting softer demand in certain areas, while industrials struck a cautious tone about the months ahead. The overall impression was of a market where some sectors basked in sunshine while others dealt with clouds.

For traders, this underscored the value of diversification: pairing growth exposure in technology with defensive positions in financials or consumer staples.

What it means for traders

The big lesson from Q2 is that corporate America is still growing strongly, but volatility is here to stay. For traders, the challenge is balancing optimism with caution.

Opportunities lie in companies that beat expectations but experience short-term pullbacks – Nvidia being a textbook case. Defensives such as Walmart continue to act as hedges against uncertainty.

ETFs provide an efficient way to capture these themes without concentrating risk too heavily. And, importantly, guidance should not be overlooked: forward-looking statements often move markets more than historical numbers.

Looking to the road ahead, analysts expect earnings to grow by 9–10% for 2025, but political and macro risks – from tariffs to elections – will shape how that plays out. In trading terms, preparation is everything. Those who monitor sentiment, manage risk, and adapt to rotation can turn volatility into opportunity.

Q2 proved that traders can thrive with the right moves. If you are ready to act on Q3 opportunities, open a live account with VT Markets to access professional tools and low-cost trading – ideal for capturing insights from earnings season.

{kind=link}