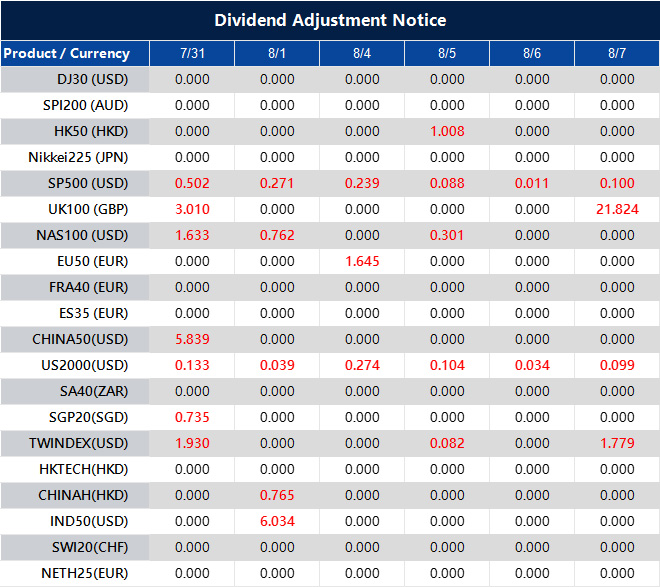

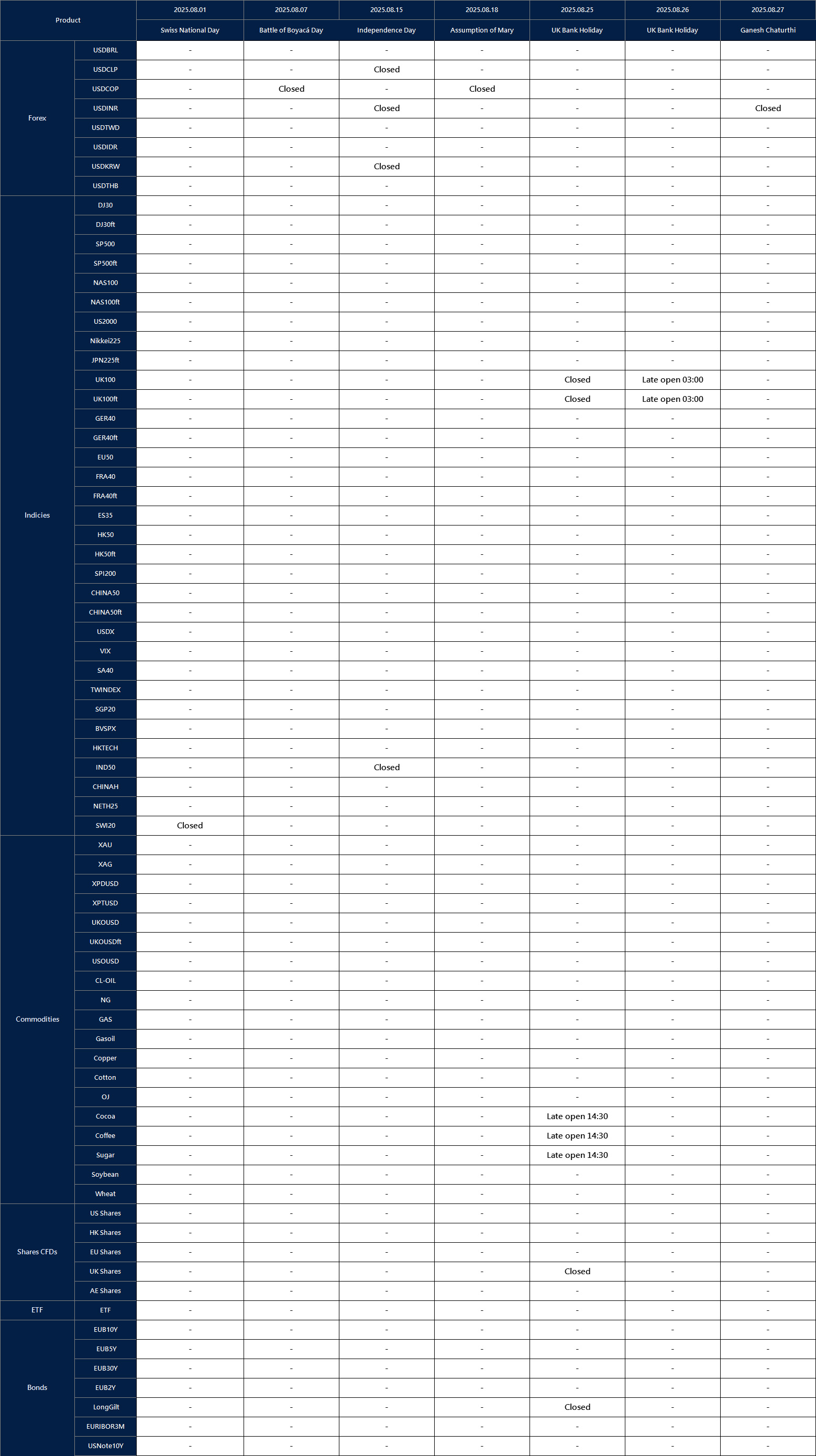

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Investor caution is building in Japan as markets await the Bank of Japan’s policy decision amid ongoing global trade tensions. With inflation expectations in focus and export risks still in play, traders are holding back, keeping the market in a narrow, uncertain range.

Markets mixed as Bank of Japan decision nears

Japanese equities closed Wednesday’s session on a mixed note, with investors taking a cautious stance ahead of the Bank of Japan’s (BOJ) upcoming monetary policy announcement.

The Nikkei 225 edged down by 0.05%, settling at 40,625.15, while the broader Topix Index rose 0.4% to 2,920, supported by gains in the banking and energy sectors.

The Bank of Japan is expected to keep its benchmark interest rate steady and boost its inflation outlook, as investors look for hints of another rate hike this year after a US-Japan trade deal reduced some uncertainty https://t.co/Q3KRaJEOU6

Market uncertainty centred around Thursday’s BOJ policy meeting. Although most analysts anticipate no change in interest rates, traders are closely monitoring for any upward revisions in the central bank’s inflation forecasts.

Persistent inflationary pressures, particularly in food and services, could push the BOJ closer to tightening policy later in the year. However, policymakers remain wary of potential global trade disruptions.

Adding to the cautious sentiment, U.S. Commerce Secretary Howard Lutnick confirmed that the 1 August tariff deadline will remain in effect for nations lacking formal trade agreements.

While an extension of the trade truce between the United States and China appears likely, no official deal has been announced. As a major export-driven economy, Japan remains vulnerable to volatility in global manufacturing and supply chains.

Technical analysis: Nikkei 225 struggles for direction

The Nikkei 225 index showed little directional commitment, retracing an intraday surge that briefly touched 40,962.15.

The index now fluctuates around its 5-, 10-, and 30-period moving averages, all of which are starting to flatten – a classic sign of market indecision or the onset of a consolidation phase.

Momentum indicators also reflect the current uncertainty. The MACD histogram continues to alternate weakly between positive and negative territory, with the signal line hovering near the zero level, offering no clear trend signal.

Picture: Nikkei 225 holds range as bulls and bears tug for direction, as seen on the VT Markets app.

With Japan’s corporate earnings season ongoing and the BOJ likely to maintain its accommodative monetary policy stance, equity investors are hesitant to take strong positions.

In the near term, the Nikkei 225 may remain range-bound between 40,550 and 40,950. A decisive breakout above the 41,000 mark could signal bullish continuation, while a drop below 40,540 may prompt a shift in sentiment towards the downside.

Market outlook: Cautious sentiment prevails

Investor sentiment remains tentative as markets await clarity from the Bank of Japan. Should the BOJ adopt a more hawkish tone or sharply upgrade its inflation projections, Japanese equities – particularly the Nikkei 225 – could face renewed selling pressure.

A strengthening yen in response to tighter policy expectations would likely add to that downward momentum, especially in export-heavy sectors.

Technically, the index is hovering near key support levels. A confirmed drop below the 40,560 zone could trigger a deeper correction, potentially targeting the 40,400 area in the short term.

This would reflect a loss of near-term confidence and might invite further selling from momentum-driven traders.

On the upside, sustained bullish sentiment would need a clear break above 40,800, ideally accompanied by strong earnings reports, improved global risk appetite, or dovish cues from the BOJ.

Until such catalysts emerge, sideways movement within the current range remains the most likely scenario.

Gamma squeezes are one of the most exciting and volatile phenomena in the stock market. When triggered, they can lead to dramatic price movements, creating significant opportunities for traders to capitalize on. But what exactly is a gamma squeeze? How does it happen, and what can traders do to navigate these intense market conditions? In this article, we’ll break down the concept of a gamma squeeze, how it works, notable examples, and key strategies to trade effectively during these explosive price surges.

What is a Gamma Squeeze?

A gamma squeeze is a market phenomenon that occurs when the price of a stock increases rapidly due to the actions of market makers involved in options trading. This happens when there is a large influx of call options being purchased on a particular stock, which leads to an increase in the stock’s price. A call option gives the buyer the right, but not the obligation, to purchase a stock at a specific price (the strike price) within a set period. When many traders buy call options, it creates a demand for the underlying stock, causing its price to rise.

Market makers—financial entities that provide liquidity by buying and selling options—are obligated to sell these call options to traders. However, because they are exposed to the risk of the stock’s price rising (since the options give the buyer the right to purchase the stock at the strike price), they need to hedge their positions. To do this, market makers buy the underlying stock, which helps to neutralize their risk. This process of buying shares to hedge against the increasing likelihood that the options will be exercised leads to a further increase in the stock’s price.

As the stock price continues to rise, the delta of the call options increases. Delta refers to the rate at which an option’s price changes relative to changes in the price of the underlying stock. For example, if the stock price rises, the delta increases, meaning that for every unit of stock price movement, the market maker must buy even more shares to maintain their neutral position. This creates a feedback loop, where the increasing price forces the market makers to buy more, which drives the price even higher, causing more options to be exercised, and so on.

This loop of rising prices continues until the gamma squeeze runs its course. The resulting price movement can be dramatic and volatile, often leading to significant swings in the stock price within a short period. The squeeze typically subsides once the options expiration date arrives, or once the demand for call options decreases. While gamma squeezes can result in massive short-term profits for those who capitalize on the price movement, they also carry high risk due to the volatility involved.

What Causes a Gamma Squeeze?

A gamma squeeze is typically caused by a combination of three factors: high options volume, rising open interest in call options, and the need for market makers to hedge their positions. Here’s a breakdown of the primary factors that contribute to this phenomenon:

1. Options Volume and Open Interest

When a large number of call options are bought at a particular strike price, the increased trading volume can influence the option price and attract more traders’ attention. Market makers (who often sell these options) must hedge their positions by purchasing the underlying asset. The more call options traded, especially at key strike prices, the greater the buying pressure on the underlying stock.

2. Delta and Gamma

The key options “Greeks” involved are delta (the rate of change in an option’s price relative to the underlying asset) and gamma, which measures the rate of change of delta as the underlying stock price moves. The relationship between the stock price and the option’s strike price, especially the call option’s strike price, is crucial in determining how much hedging is required. As the stock price rises and approaches or surpasses the option’s strike price, delta increases, forcing market makers to buy even more stock to maintain their hedges. This gamma effect, as gamma measures the sensitivity of delta to price changes, can drive the stock price further up.

3. Market Sentiment

Often, a gamma squeeze is driven by speculative buying, especially in volatile markets, as traders act on expectations of future price movements in the underlying stock. Retail traders or large institutional players may push the stock price higher, contributing to a self-perpetuating cycle of buying.

The Key Players Involved in a Gamma Squeeze

Understanding the key participants in a gamma squeeze is crucial to identifying the forces driving the market:

Market Makers: These are the financial entities responsible for providing liquidity in the options market. They sell options contracts to traders and hedge their risk by buying or selling the underlying stock. When a gamma squeeze occurs, market makers are forced to buy more shares of the underlying stock to balance their positions, which drives the stock price higher.

Retail Traders: Retail traders often contribute to a gamma squeeze by buying call options in large quantities. As their activity increases, they create the buying pressure that leads to a significant rise in the stock price.

Institutional Investors: While gamma squeezes are often triggered by retail traders, institutional investors can play a role in amplifying the event. Large institutional players may contribute to the rally by buying additional options or shares, further driving the squeeze.

Gamma Squeeze vs. Short Squeeze: What Are the Key Differences?

While both gamma squeezes and short squeezes can result in dramatic price movements, they occur through different mechanisms and involve different market dynamics. The table below shows the key differences between a gamma squeeze and a short squeeze, helping to clarify how each one operates and the forces behind them.

Aspect

Gamma Squeeze

Short Squeeze

Trigger Mechanism

Driven by the buying of call options and the hedging actions of market makers.

Caused by short sellers being forced to buy back shares to cover their positions.

Price Movement

Rising stock price forces market makers to buy more shares to hedge their options positions, driving the price even higher.

A high level of short interest and an unexpected price rise.

Market Players

Short sellers, retail investors, and hedge funds who are betting against the stock.

Rising stock prices forces short sellers to buy back stock, causing a further price increase.

Driving Factor

Surge in call options buying and hedging needs of market makers.

It can last as long as short sellers struggle to cover their positions, often triggered by news or events.

Timeframe

Typically short-term but can be quick and volatile, lasting until options expiration or price correction.

Can last as long as short sellers struggle to cover their positions, often triggered by news or events.

Outcome

A feedback loop of rising prices due to continuous hedging; in some cases, the stock rose dramatically due to a gamma squeeze.

A rapid price increase caused by short sellers being squeezed out of their positions.

Gamma Squeeze: A gamma squeeze is triggered when there is significant buying activity in call options. Market makers, who sell these options, are required to hedge their positions by purchasing the underlying stock. As the stock price rises, market makers need to buy even more shares to adjust their hedge, creating a feedback loop of increasing prices.

Short Squeeze: A short squeeze, on the other hand, happens when short sellers—who have bet against a stock—are forced to buy back shares to cover their positions as the price unexpectedly rises. This buying pressure from short sellers further drives the price higher, triggering even more buying.

While both squeezes are driven by a surge in buying pressure, the key difference is in the cause: a gamma squeeze is driven by options traders and the need for market makers to hedge, while a short squeeze is caused by short sellers scrambling to cover their positions.

A gamma squeeze can lead to dramatic price movements, as shown in these notable examples, where the buying of call options triggered significant surges in stock prices due to the hedging activities of market makers.

1. GameStop (GME) – January 2021

The GameStop gamma squeeze is perhaps the most famous example of a gamma squeeze that also triggered a short squeeze. Retail traders, primarily from the Reddit group WallStreetBets, began buying massive quantities of out-of-the-money GameStop call options, which led to a surge in options volume. Market makers, who sold these options, were forced to buy GameStop stock to hedge their positions. This created a feedback loop where the rising stock price forced market makers to buy even more shares, causing the price to skyrocket from under $20 to over $400 in a matter of days. The gamma squeeze was further intensified by high short interest in GameStop, leading to a combination of both a gamma squeeze and a short squeeze.

2. AMC Entertainment (AMC) – May 2021

Similar to GameStop, the AMC gamma squeeze occurred in May 2021. AMC gamma squeeze explained: This event was driven by retail traders, particularly from online communities like Wall Street Bets, who bought up a large number of call options for AMC stock. This activity played a crucial role in preventing AMC’s bankruptcy during the COVID-19 crisis. As the price rose, market makers had to buy more shares to hedge, fueling the price increase even further. AMC’s stock, which had been trading around $5 to $10, soared to over $60 within a matter of weeks. The high demand for call options and the associated buying pressure created a classic gamma squeeze scenario.

3. Volkswagen (VW) – October 2008

One of the most remarkable examples of a gamma squeeze took place with Volkswagen (VW) stock in October 2008. During this time, Porsche revealed that it had acquired a majority of the outstanding shares of Volkswagen, putting pressure on short sellers. In response, many traders bought call options to capitalize on the potential rise in Volkswagen’s stock price. Market makers, who sold the options, were forced to hedge by buying more shares, driving the price of Volkswagen stock up from around €200 to over €1,000 within just a few days. This squeeze became one of the most extreme price movements in stock market history.

4. SoftBank (SFTBY) – 2020

Another significant gamma squeeze occurred in 2020 when SoftBank, a Japanese conglomerate, became a large player in the options market. The company made massive purchases of call options on various tech stocks, which sparked a rise in their prices. As the prices of stocks like Amazon, Apple, and Tesla began to surge, market makers were forced to buy more shares to hedge their positions, further escalating the price increases. This created a gamma squeeze that affected several high-profile stocks in a short period of time, showcasing the power of options in driving stock prices.

How to Spot a Gamma Squeeze

A gamma squeeze can be tricky to identify, but there are several indicators that can signal its onset.

1. Unusual Options Volume

One of the first signs of a potential gamma squeeze is a surge in call options volume. If you notice a significant increase in the number of out-of-the-money (OTM) call options being traded, particularly at the same strike price, it’s likely that market makers will need to hedge their positions. This can lead to increased buying pressure on the underlying stock.

2. Rising Open Interest

Look for a rapid increase in open interest for call options. When traders buy calls, especially in large quantities, it forces market makers to purchase more stock to hedge against potential price moves. This can amplify the gamma squeeze effect.

3. Increase in Implied Volatility

A sharp rise in implied volatility (IV) can signal that the market expects significant price movement. As IV rises, market makers may buy more of the underlying stock to hedge their positions, adding to upward price pressure and potentially triggering a gamma squeeze.

4. Rapid Price Movements

Watch for fast price increases without corresponding news or earnings reports. If the price rises quickly alongside increased options activity, it’s a strong indication that a gamma squeeze might be at play, as market makers scramble to hedge their options exposure.

How to Trade During a Gamma Squeeze

Trading during a gamma squeeze can be profitable but requires understanding the market dynamics. Here are the key steps to trade effectively during a gamma squeeze:

Step 1: Monitor Options Activity

Watch for high call options volume and rising open interest, which signal a potential gamma squeeze.

Step 2: Buy Call Options

If a gamma squeeze is forming, buying call options can offer high returns as the stock price rises. Opt for at-the-money options and be mindful of expiration.

Step 3: Enter the Stock Market

If you prefer buying the stock, enter when the price begins rising sharply. Timing is crucial—avoid entering too early or too late.

Step 4: Use Stop-Loss Orders

Protect your position with a stop-loss or trailing stop as the price rises to lock in gains while allowing for further movement.

Step 5: Take Profits

Exit the position when the price hits resistance or volume drops. Gamma squeezes are short-lived, so capitalize on the surge before it fades.

Step 6: Stay Alert for Reversals

Watch for quick price reversals after the squeeze peaks. Exit or hedge if the price starts to fall rapidly to protect your gains.

Key Considerations When Trading a Gamma Squeeze

Trading a Gamma Squeeze can be profitable, but it requires careful strategy. Here are the key considerations for trading a gamma squeeze effectively:

Volatility: Gamma squeezes are often short-lived, with prices potentially experiencing sharp reversals. Traders should be aware of the risks and ready to exit positions quickly.

Emotions: FOMO (Fear of Missing Out) can drive irrational trading behavior during gamma squeezes. Traders should stick to their strategies and avoid chasing the rally.

Liquidity: Ensure there is enough liquidity in the stock or options you’re trading to avoid large slippage when entering or exiting positions.

Timing: Timing is crucial. Gamma squeezes often happen quickly, and traders must be able to enter and exit the market efficiently to lock in profits.

A gamma squeeze occurs when a surge in call options buying forces market makers to hedge by buying the underlying stock, creating a feedback loop that drives prices higher. While trading during a gamma squeeze can be profitable, it’s essential to carefully monitor options activity, open interest, and stock price movements to manage risk effectively. Understanding the dynamics of the squeeze and timing your entry and exit points is crucial for maximizing profits.

A gamma squeeze occurs when a surge in call options buying forces market makers to buy more of the underlying stock to hedge their positions, driving the price higher.

2. What causes a gamma squeeze?

A gamma squeeze is caused by the rapid buying of call options, which forces market makers to buy the underlying asset to hedge their positions, driving the price higher.

3. How is gamma squeeze different from a short squeeze?

A gamma squeeze is driven by options buying and hedging, while a short squeeze occurs when short sellers are forced to buy back stock to cover their positions.

4. Can a gamma squeeze happen in any market?

Yes, a gamma squeeze can occur in any market where options are traded, but it’s more common in stocks with high volatility or speculative interest.

5. How does a gamma squeeze affect stock prices?

As market makers buy more stock to hedge their options, the increasing demand causes the stock price to rise, creating a feedback loop that drives prices even higher.

6. How to spot a gamma squeeze?

To spot a gamma squeeze, traders should monitor the following indicators:

Unusual options volume

Rising open interest

Increase in implied volatility

Rapid price movements

7. How to trade during a gamma squeeze?

Here are the key steps to trade effectively during a gamma squeeze:

Step 1: Monitor options activity

Step 2: Buy call options

Step 3: Enter the stock market

Step 4: Use stop-loss orders

Step 5: Take profits

Step 6: Stay alert for reversals

8. How long does a gamma squeeze typically last?

A gamma squeeze can last anywhere from a few hours to several days, depending on the level of options activity and market dynamics. It often ends when the options expiration date arrives or when the buying pressure diminishes.

9. Can a gamma squeeze happen with any stock?

While it’s possible for a gamma squeeze to occur with any stock, it’s more common in stocks with high volatility and significant options trading activity.

10. Can retail traders cause a gamma squeeze?

Yes, retail traders can drive a gamma squeeze by buying large volumes of call options, which increases demand for the underlying stock and triggers the hedging actions of market makers.

11. What are the risks of trading during a gamma squeeze?

The main risk is that gamma squeezes are often short-lived, and prices can reverse quickly. If you’re caught in the wrong position, you could face significant losses.

12. How can I protect myself when trading a gamma squeeze?

To protect yourself, use stop-loss orders, stay alert to price movements, and consider using hedging strategies like buying puts or selling call options to manage risk.

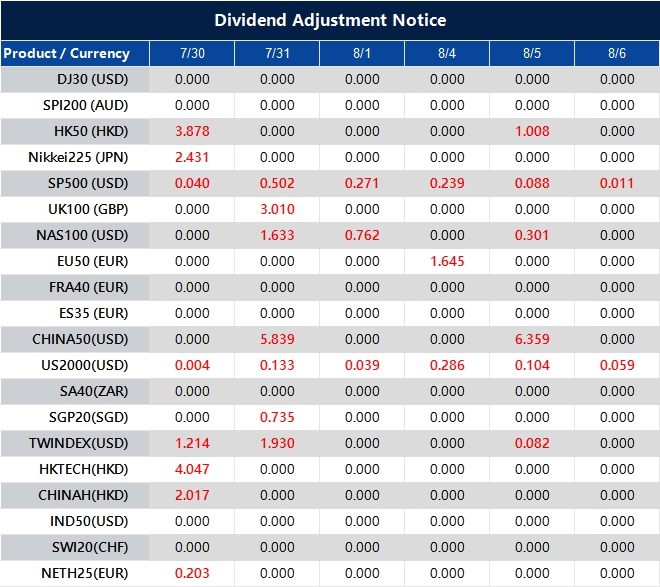

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

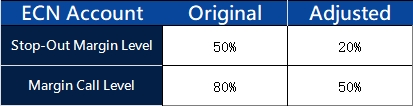

To provide our valued clients with an enhanced trading environment, VT Markets will adjust certain trading conditions for ECN account on August 2, 2025:

Friendly reminder:

1.All account settings stay the same except for the above adjustments.

2.All account types now have the same Stop-Out and Margin Call Level.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Trade tensions and political uncertainty have weighed on the euro this week, while the US dollar gained strength on safe-haven demand and renewed global engagement. With central bank guidance and policy risks in focus, EUR/USD remains under pressure.

Euro under renewed pressure

The euro struggled to recover this week following Monday’s sharp 1.3% decline – its steepest one-day drop in over two months.

EUR/USD was last seen trading at $1.1594, rising only 0.07% as markets absorbed the broader implications of the newly ratified US-EU trade agreement.

The EU dodged an imminent trade war with the US this week, but markets and a growing chorus of critics have dispelled early hopes that the deal will bring a sense of stability back to transatlantic relations https://t.co/xDfQfplSqJ

The deal triggered political backlash across Europe. French officials condemned it as a “dark day” for the continent, while German Chancellor Friedrich Merz warned that the 15% base tariff on EU exports could cause significant harm to Germany’s export-driven economy.

Falling European bond yields added to the euro’s weakness, helping the US dollar strengthen further. The Dollar Index (USDX) gained 1% overnight to reach 98.67.

This strength also dragged the British pound to a two-month low of $1.3349 and pushed USD/JPY higher to 148.49.

Outside Europe, dollar strength was reinforced by growing signs of renewed US diplomatic engagement.

Macquarie strategist Thierry Wizman suggested the dollar’s rise reflects more than trade – it signals a wider re-engagement strategy.

President Trump also warned that countries without standalone deals may face tariffs of 15–20%, intensifying global trade uncertainty.

Meanwhile, US-China talks resumed in Stockholm, extending their trade truce by another three months.

Traders now await interest rate decisions from both the Federal Reserve and the Bank of Japan. While no changes are expected, forward guidance could shape market direction into the next quarter.

Technical analysis

EUR/USD remains in a clear downtrend after peaking near 1.1770, forming a series of lower highs and lower lows over recent sessions.

Both the 5- and 10-period moving averages are sloping downward, confirming continued bearish momentum.

Price is currently trading just beneath these short-term averages, highlighting sustained selling pressure.

Picture: EUR/USD breaks below key support after a relentless downtrend from 1.1770, as seen on the VT Markets app.

Although the MACD remains in negative territory, the histogram bars are beginning to contract slightly – indicating a possible, albeit limited, slowdown in downward momentum.

A decisive move below 1.1580 could open the door to further losses toward the 1.1530 support area.

On the upside, a break above 1.1620 would be needed to challenge the current descending trendline and potentially shift sentiment.

Bearish outlook unless key resistance breaks

Unless EUR/USD can decisively reclaim the 1.1620 level, the pair remains vulnerable to further downside pressure, with 1.1550 seen as the next key support.

A brief consolidation may occur near this level, but any sustained recovery would likely require a clear shift in market sentiment or fresh macroeconomic catalysts.

Traders remain cautious as geopolitical tensions and trade uncertainties weigh on confidence. The euro continues to struggle amid concerns over export tariffs and the broader impact of the US-EU trade deal, which many analysts believe could undermine European competitiveness in the months ahead.

Looking ahead, forward guidance from the Federal Reserve and the European Central Bank will be closely watched.

Any signals regarding inflation outlook, interest rate timelines, or monetary policy adjustments could influence near-term price action.

As Q3 progresses, these policy cues will be crucial in determining whether EUR/USD can stabilise – or slip further into bearish territory.

In the world of trading, having the right tools to assess market trends and price movements is essential. One such powerful tool is VWAP (Volume Weighted Average Price), an indicator that provides a real-time average price of an asset, factoring in both its price and the volume of trades. Whether you’re a day trader looking to identify entry and exit points or seeking to understand market sentiment, VWAP offers valuable insights. In this article, we’ll explore what VWAP is, how it works, how to calculate it, and how traders use it to make more informed decisions in dynamic markets.

What is VWAP?

VWAP, or Volume Weighted Average Price, is a key technical indicator widely used by traders to evaluate the average price of an asset over a specific period, factoring in both its price and volume. It provides an insightful gauge of the market’s average price, considering the importance of trading volume at different price levels. In simpler terms, VWAP helps traders understand whether the price of an asset is overvalued or undervalued, making it essential for day trading and intraday analysis.

What makes VWAP unique is its inclusion of volume, which reflects the true market activity at each price level. Higher volumes at certain price points have more influence on the VWAP than lower-volume trades, making it a more accurate representation of the market’s consensus price at any given time. VWAP is a stock weighted indicator, meaning prices are weighted by trading volume to provide a more accurate market consensus. For traders, VWAP is an essential tool to determine whether an asset is overvalued or undervalued, especially in the context of day trading and intraday analysis. It is especially useful for identifying trends, entry points, and exit points in a fast-moving market.

How VWAP Works

VWAP operates by calculating the average price of an asset throughout the trading day, weighted by the volume of each trade. It is updated in real-time during the trading session and reflects the true value of a stock, incorporating both price and trading volume. Calculating VWAP involves determining the value for each data point—typically each intraday candle or bar—so that VWAP is calculated continuously as new data points are added throughout the session.

The key to understanding how VWAP works is recognizing its reliance on volume. A larger trading volume at a specific price point results in a greater influence on the VWAP, making it more relevant in evaluating the price action of an asset. VWAP is calculated using the price and volume of each data point within a defined period, and the calculation maintains a running total of price-volume values throughout the session. For example, if a stock experiences a high volume of trades at $100, that price point will have a more significant impact on the VWAP than trades at $95 with lower volume. VWAP is calculated by aggregating these values over the selected period.

Formula for VWAP

VWAP is updated continuously during the trading day, providing a running average that reflects both the price and volume of an asset. The formula for VWAP is as follows:

VWAP = Sum of (Typical Price × Volume) / Total Volume Traded

Where:

Typical price is calculated as the average of the high, low, and closing price for each interval.

Closing price is one of the components used to determine the typical price.

Volume is the number of shares or contracts traded at that price point.

Total volume traded refers to the sum of all shares or contracts traded during the period.

VWAP is calculated using the typical price for each interval, multiplied by the volume, summed across all intervals, and then divided by the total volume traded during the period. This process results in a running average, updated throughout the trading session.

How to Calculate VWAP

To calculate VWAP accurately throughout the trading day, follow these steps:

Calculate the average price, also known as the typical price, for each trading period (e.g., 5-minute window) by adding the high, low, and closing price for that period and dividing the sum by three: (high + low + closing price) / 3. This gives the typical price for that specific period.

Multiply the typical price by the volume traded during that period. This is called Price × Volume (PV).

Each period represents a data point in the calculation. Record the PV value for each data point, then add the PV values from all data points throughout the day.

Divide the running total of PV by the cumulative, or total volume traded up to that point. This provides you with the updated VWAP for the day.

How Traders Use VWAP

Traders use VWAP in various ways to enhance their trading strategies, particularly for intraday trading. Here’s how VWAP can be applied:

1. Trend Identification

VWAP helps traders identify the overall market trend. When the current price is above the VWAP, it generally indicates a bullish market, as it shows that buyers are in control. Conversely, when the price is below the VWAP, it suggests a bearish trend, indicating that sellers are dominant. A downward trend is characterized by prices consistently trading below the VWAP, signaling ongoing selling pressure.

Example:

For major currency pairs like EUR/USD, if the price is trading at 1.2100 while the VWAP is at 1.2050, it indicates that the price is above the VWAP, suggesting a bullish trend. Traders may interpret this as a sign that buying pressure is stronger than selling pressure. However, if the price begins to decline and drops to 1.2000, falling below the VWAP, it could signal a potential reversal to a bearish trend, indicating that sellers are gaining control of the market.

2. Entry and Exit Points

VWAP can serve as a support or resistance level for price movements during the day. Traders use these levels to decide the best time to enter or exit positions. When the price approaches the VWAP from below, it may act as a support level. When the price moves toward VWAP from above, it may serve as a resistance level.

Example:

For commodities like gold (XAU/USD), suppose the price has been rising steadily and reaches $1,825, while the VWAP is at $1,810. If the price starts to pull back and approaches the VWAP at $1,810, traders may view this as a support level. If the price holds above this level and starts to rise again, it could be an ideal entry point for a long position, with the expectation that the uptrend will continue. However, if the price fails to hold above the VWAP and moves lower, this could signal the end of the uptrend, and traders might exit or short the position.

3. Volume Confirmation

VWAP helps traders confirm the strength of a trend by considering the volume of trades at each price level. High trading volume at specific price levels typically indicates stronger market participation, which makes the trend more reliable. Conversely, low volume during price movements can signal a weak trend that may not be sustainable.

Example:

In Tesla (TSLA), suppose the stock breaks above the VWAP at $650 with significantly higher volume than its average. This suggests that the breakout is supported by strong buying interest, confirming the strength of the trend. Traders might interpret this as a good signal to enter long positions. However, if the price of Tesla moves above the VWAP at $650, but the volume is relatively low, it may indicate that the price move lacks conviction. In this case, traders may hesitate to enter or may even decide to wait for a clearer signal before making a move.

Advantages and Disadvantages of VWAP

While VWAP is a valuable tool for traders, there are both advantages and disadvantages to using it:

Advantages:

Volume-Weighted Insight: VWAP takes into account both price and trading volume, providing a more accurate representation of an asset’s value. This helps traders understand the market’s true sentiment and make better-informed decisions.

Trend Confirmation: VWAP is an excellent tool for confirming the prevailing trend. When prices are above VWAP, it signals a bullish market, while prices below VWAP indicate bearish sentiment, helping traders spot potential entry and exit points.

Support and Resistance: VWAP acts as a dynamic support and resistance level, providing traders with a reliable benchmark to identify key levels where the price might reverse or continue its movement.

Disadvantages:

Intraday Limitation: VWAP is most useful for intraday trading and resets at the start of each trading day. It is not effective for long-term trend analysis, which makes it less suitable for swing traders or position traders.

Not a Predictive Indicator: VWAP tracks past price and volume data, which means it doesn’t predict future price movements. It’s helpful for understanding market trends, but should be used with other tools for more comprehensive analysis.

Less Effective in Volatile Markets: During periods of high volatility, VWAP might give conflicting signals as prices can rapidly move away from the VWAP, leading to false interpretations. In such markets, traders may need to adjust their strategies accordingly.

Weighs periods with higher trading volumes more heavily.

Treats all prices equally without considering volume.

Time Sensitivity

Resets daily, suitable for intraday trading.

Calculated for a set period, suitable for both short- and long-term analysis.

Usage

Best for intraday trading and short-term analysis.

Applicable for both short-term and long-term trading strategies.

Volume Sensitivity: VWAP differs from moving averages in that it gives more weight to periods with higher trading volumes. This makes VWAP a more accurate reflection of price action, especially for assets that experience varying liquidity levels. Moving averages, on the other hand, treat every price point equally, which can make them less reliable in markets with fluctuating volumes.

Time Sensitivity: Unlike moving averages, which are calculated over a fixed period (e.g., a 20-day SMA), VWAP resets at the start of each new trading day. This makes VWAP particularly useful for intraday trading, as it provides a real-time measure of an asset’s price action throughout the day. Moving averages, however, are typically used to track trends over longer periods, such as days, weeks, or months, making them suitable for both short-term and long-term trading strategies.

Usage: VWAP is primarily used by day traders and intraday traders because it resets every day and provides a real-time weighted average. This makes it ideal for assessing short-term trends. Moving averages are more versatile and can be applied to both short-term and long-term strategies, helping traders track broader trends over a set period.

Common Mistakes When Using VWAP

While VWAP is a powerful tool, there are some common mistakes traders should avoid:

Overreliance on VWAP: Traders sometimes rely solely on VWAP without considering other indicators or market conditions. This can lead to poor decision-making. It’s essential to use VWAP in combination with other tools like RSI or MACD for a more complete analysis.

Ignoring Volume: Since VWAP is volume-weighted, neglecting the volume aspect can lead to false signals. For instance, a price move without strong volume backing it may not be as significant as it appears. Always consider both price and volume for more accurate insights.

Misinterpreting in Trending Markets: In strong uptrends or downtrends, VWAP may act as dynamic support or resistance. Relying on it without considering the strength of the trend can result in missed opportunities or wrong decisions. Traders should adjust their strategy accordingly.

Using VWAP in Isolation: While VWAP is useful for intraday trading, using it in isolation without a broader market context can lead to confusion. Traders should factor in overall market conditions and other technical indicators to ensure they’re making informed decisions.

In Summary

VWAP is a valuable indicator for traders looking to analyze intraday price action by considering both price and volume. It offers insights into market sentiment, supports decision-making for entry and exit points, and can help traders identify potential trends. However, like any indicator, it should be used in conjunction with other analysis tools for the best results.

Start Trading Today with VT Markets

Are you ready to integrate VWAP into your trading strategy? VT Markets provides access to advanced charting tools, competitive spreads, and a wide range of assets to trade. Whether you prefer MetaTrader 4 (MT4) or MetaTrader 5 (MT5), our platforms offer real-time market data and powerful tools to enhance your trading decisions. If you’re new to trading, you can explore our VT Markets demo account to practice with virtual funds before going live. Our Help Centre is also available to guide you through the process, ensuring you have all the support you need to succeed.

VWAP stands for Volume Weighted Average Price. It is a technical indicator that calculates the average price of an asset throughout the day, weighted by trading volume. It is used to assess the true value of an asset, as it takes both price and volume into account, providing a more accurate reflection of market activity compared to other price-based indicators.

2. What is the difference between VWAP and moving averages?

VWAP is a volume-weighted average price, whereas moving averages (SMA/EMA) give equal weight to all prices, regardless of volume. VWAP is more suited for intraday trading.

3. Can VWAP be used in long-term trading?

No, VWAP is mainly used for intraday analysis and resets every day, making it less suitable for long-term trading.

4. How often should traders update their VWAP calculations?

VWAP is updated in real-time throughout the trading day, so traders should monitor it continuously during market hours.

5. How can VWAP help identify market trends?

VWAP helps identify whether a market is in an uptrend or downtrend. When the price is above the VWAP, it typically indicates a bullish market, while prices below the VWAP suggest a bearish trend. A downward trend is indicated when prices remain below the VWAP for an extended period.

6. Can VWAP be used for all types of assets?

Yes, VWAP can be applied to a wide range of assets, including stocks, forex, precious metals, and cryptocurrencies. However, it is particularly popular in intraday trading due to its real-time updates.

7. How do traders use VWAP for entry and exit points?

Traders use VWAP as a support or resistance level. If the price approaches VWAP from below, it may act as a support level to buy, and if it approaches from above, it may act as a resistance level to sell.

8. What is the best way to combine VWAP with other indicators?

VWAP works well in conjunction with momentum indicators like RSI or MACD to confirm the strength of a price move, or with trend indicators like moving averages to assess the overall trend direction.

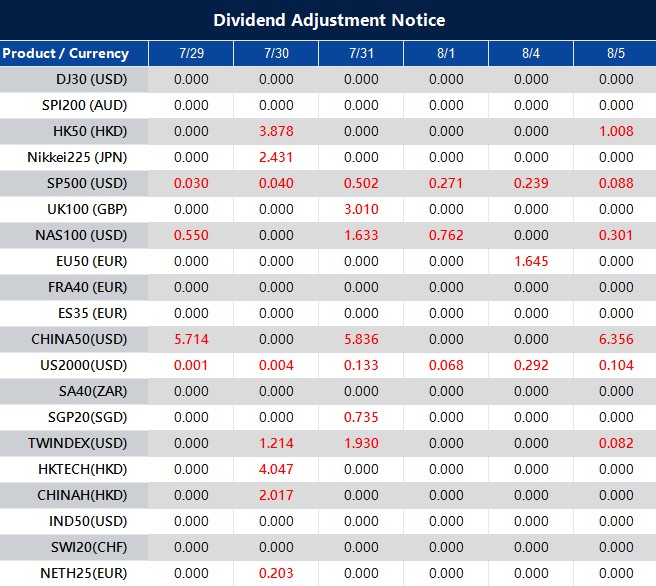

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact info@vtmarkets.com.

Affected by international holidays, the trading hours of some VT Markets products will be adjusted. Please check the following link for the affected products:

Crypto markets started the week on a positive note, driven by easing trade tensions and fresh progress on US regulation. As lawmakers work to clarify the legal status of digital assets, investor confidence is improving, setting the stage for potential short-term gains.

Bitcoin up on hopes of easing regulation

Bitcoin kicked off the week on a positive note, climbing 0.8% to $119,026, according to CoinDesk.

The rally comes as global trade tensions show signs of easing, and the US makes strides in establishing clearer cryptocurrency regulations.

Meanwhile, Ether rose 3.3% to $3,890, XRP advanced 2.6% to $3.27, and Solana gained 2.7% to reach $192.21.

In broader markets, equity futures edged higher – S&P 500 futures were up 0.3%, and Nasdaq futures rose 0.5%.

Much of Bitcoin’s recent support has been linked to improving global sentiment following President Donald Trump’s announcement of a 15% base tariff on EU imports.

While the new measure maintains certain trade limitations, it has largely been perceived by investors as a stabilising move – particularly for risk assets like cryptocurrencies.

European capitals are putting a brave face on the trade deal they struck with President Donald Trump, which will see the European Union accept a 15% tariff on most of its exports to the US while reducing levies on some American products to zero https://t.co/8Xxn0ncTWF

Additionally, progress on US crypto regulation has further boosted market confidence. The Genius Act – now enacted into law – provides formal recognition of stablecoins as legitimate financial instruments pegged to traditional fiat currencies.

"Ethereum is the largest beneficiary of the Genius Act, which is the stablecoin bill, because ethereum hosts is home to the majority of stablecoins," The Ether Machine co-founder @AK_EtherMachine says. pic.twitter.com/DAiT62iTX9

More critically, the House passed the Clarity Act, a long-awaited bill aimed at defining whether cryptocurrencies are to be treated as commodities or securities.

This legal clarity is expected to attract increased interest from institutional investors who have remained on the sidelines due to regulatory uncertainty.

Technical analysis

Bitcoin has entered a consolidation phase after reaching a recent intraday high of $119,800.64.

Despite initial bullish momentum, the price has since lost steam and is now hovering just below the 10- and 30-period moving averages on the 15-minute chart.

Picture: BTC/USD retraces after testing $119,800 resistance, as seen on the VT Markets app.

A bearish crossover between the 5- and 10-period moving averages beneath the 30-MA signals a decline in upward strength.

The MACD has also turned negative – its main line has dipped below the signal line, and the histogram is growing increasingly bearish. These signals suggest growing downward pressure.

BTC continues to test a key support zone around $118,700, which has so far held firm. However, a decisive break below this level could trigger a further drop towards $118,200.

For bulls to regain control, the price would need to reclaim $119,800 with strong volume, ideally confirmed by a bullish MACD crossover.

Short-term forecast: Cautious optimism

Bitcoin’s ability to hold above the $118,700 support level remains a key factor in the near-term outlook.

Should this level continue to provide a solid floor, the price may attempt another push toward the psychologically significant $120,000 mark.

However, the path upward appears less certain, as short-term technical indicators are showing signs of fatigue.

The MACD is trending lower, and moving averages on the intraday chart are beginning to flatten – both signals suggesting that bullish momentum is weakening.

While a breakout above $120,000 is still within reach, any move higher is likely to be slow and methodical rather than explosive.

Traders and investors may remain cautious until there is greater clarity on the regulatory front. Much will depend on how the Senate responds to the Clarity Act when it reconvenes.

A supportive stance could reignite market enthusiasm, especially among institutional players who have long awaited a definitive legal framework.

Until then, BTC may continue to trade within a tight range, with sentiment fluctuating based on macroeconomic news and policy signals from Washington.

| VT Markets")

| VT Markets")

| VT Markets")

{kind=link}