The display industry once built some of the world’s most advanced manufacturing infrastructures — massive cleanrooms, precision lithography lines, and glass-handling systems — all to produce screens that became ubiquitous in smartphones, TVs, laptops, and out-of-home digital signage. For decades, these displays powered everything from living rooms to billboards, yet the business gradually became commoditised, with tight margins and fierce global competition.

Today, AI is giving this infrastructure a second life: it’s powering intelligent factory floors, enabling advanced semiconductor packaging, and even converting entire panel factories into data centres. What was once a survival-of-the-cheapest business is now being repurposed for survival-of-the-smartest.

The Factory Floor Just Changed Hands

At SID Display Week 2026 in Los Angeles, BOE Technology Group hosted the display industry’s first AI+ forum, unveiling its “AI Plus” strategy built around the Blue Whale Foundation Model for manufacturing, products, and operations. Over 30 world-first or industry-first innovations were on show, with 65% being industry debuts. The centrepiece wasn’t a panel. It was an AI-powered production system handling defect detection, supply chain risk, quality management, and energy optimisation across BOE’s factory network.

BOE wasn’t alone. SID itself noted that AI is now applied across the entire display development process, from materials discovery to manufacturing yield and real-time performance optimisation. Samsung Display, LG Display, TCL CSOT, and Visionox all showcased AI-integrated solutions. The message from the industry’s largest annual gathering was unanimous: panel makers are no longer just shipping screens.

Weeks earlier, a more telling signal came from The Elec. Samsung Display and LG Display are reviewing glass interposer opportunities in the advanced semiconductor packaging market, as AI chip demand drives persistent shortages in 2.5D and 3D packaging capacity. Display companies aren’t just automating their existing business. They’re exploring entry into the semiconductor supply chain itself.

From Cleanrooms to Server Racks

To understand why this matters, consider the industry’s past:

- Japan dominated LCD manufacturing. Sharp’s Sakai factory, opened in 2009, was the world’s first tenth-generation plant. In the early 2010s, Japanese companies controlled over 40% of global LCD market share.

- China entered the fray. BOE and TCL Huaxing built massive factories supported by government subsidies, triggering a price war. By 2025, China dominated global LCD production, pushing Japanese panel makers to the margins.

The response has been dramatic. Sharp’s Sakai site, once called the “LCD capital”, is being converted into AI data centre space, with rows of server racks replacing the cleanrooms where panels used to be made. That’s not a metaphor. It’s a literal repurposing of display manufacturing infrastructure for the AI era.

This is the pattern playing out across the industry, in different forms:

| Shift | What’s happening | Who |

| AI-powered manufacturing | AI handling defect detection, yield optimisation, production planning, energy management, and enabling smarter display products (eye tracking, adaptive brightness, glasses-free 3D) | BOE (Blue Whale model), Samsung (Nvidia digital twin partnership) |

| Semiconductor packaging entry | Display makers leveraging decades of glass and precision fabrication expertise to help build AI chip packaging | Samsung Display, LG Display reviewing glass interposers |

| Physical conversion | Former LCD factories repurposed as AI data centre infrastructure | Sharp (Sakai factory) |

On the demand side, AI-powered devices are pulling new panel orders.

Counterpoint reported that global AR smart glasses shipments climbed 98% for the full year 2025, with H2 shipments rising 148% year on year. Last year, IDC forecasted smart glasses category growing 247.5% during 2025, driven by AI-equipped models from Meta, Xiaomi, and emerging Chinese brands. Omdia noted that demand for mobile PCs driven by AI advancements is also contributing to display area demand growth. These are genuine pull-through demand categories indicating that AI devices need more screens.

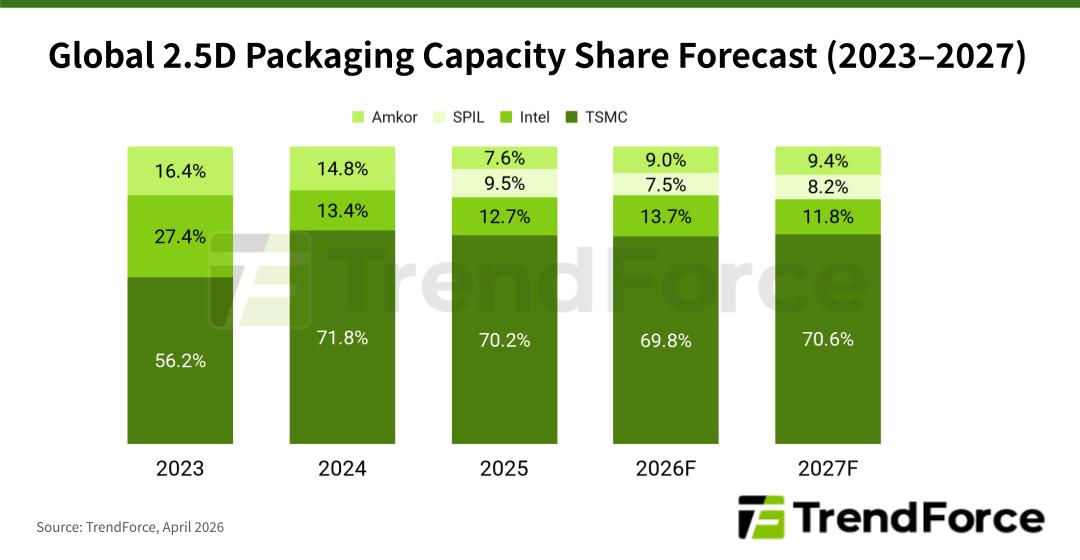

The Packaging Bottleneck

Advanced packaging has traditionally been dominated by semiconductor foundries and OSAT companies like TSMC, ASE Technology, Amkor. But display manufacturers have spent decades working with glass substrates, thin-film transistor arrays, and precision lithography at panel scale.

TSMC aims to scale monthly CoWoS (Chip-on-Wafer-on-Substrate) capacity from approximately 35,000 wafers in late 2024 to 130,000 by late 2026 — nearly quadrupling output. Even with that expansion, Nvidia alone has reportedly secured over 60% of total CoWoS capacity for 2025 and 2026. The rest of the industry is fighting for what’s left. Global advanced packaging demand reaches around 146,000 300mm wafer equivalents per month, with supply shortage rates at roughly 23% and lead times exceeding one year for some orders.

The market behind this bottleneck is scaling fast. Bloomberg Intelligence found that the market for 2.5D and 3D advanced packaging could grow eightfold to $80.5 billion by 2033, with a 26% compound annual growth rate that significantly outpaces the 10% projected growth for the overall semiconductor industry.

That gap is what’s pulling display makers in.

Decades of experience handling glass substrates, thin-film transistor arrays, and precision lithography give display businesses a foundation that overlaps directly with the requirements for fan-out panel-level packaging (FOPLP) and glass interposers. With the first commercial applications of glass-based advanced packaging expected by late 2027, the timeline for meaningful market entry is becoming increasingly clear.

Some examples illustrate how this is playing out:

- Samsung Display already bridges both industries:

- $73.24 billion semiconductor investment in 2026 across memory, foundry, and advanced packaging.

- Collaboration with Nvidia on AI Factory development, leveraging digital twin manufacturing to scale production.

- Introduction of Hybrid Copper Bonding packaging, improving thermal resistance by 20% for high-performance computing environments.

- LG Display is at an earlier stage, exploring glass interposer opportunities, signaling an early but structurally significant entry into advanced packaging.

If even one major display maker successfully executes at scale, it would validate the pathway for others, adding substantial capacity to a market that is not expected to reach supply-demand balance until after mid-2027.

The most investable part of this story isn’t AI in display factories. It’s display makers entering semiconductor packaging because the supply gap pulling them in is enormous.

A Pattern the Market Has Seen Before

This precedent has been revealed with TOTO. Earlier this year, the Japanese bathroom company’s shares jumped nearly 10% after analysts highlighted its electrostatic chucks as beneficiaries of AI-driven semiconductor demand.

TOTO didn’t become an AI company; part of its business simply sat where AI demand compounded. The market re-rated TOTO not because it became an AI company, but because part of its business sat at a manufacturing bottleneck where AI demand compounded.

Display makers are following the same arc with higher stakes.

TOTO’s ceramics business is a niche component supplier. Display companies are sitting on entire factory complexes, decades of precision fabrication expertise, and glass substrate capabilities that the semiconductor packaging industry now needs. The re-rating potential is larger, but so is the execution risk.

Building electrostatic chucks is a proven business. Entering advanced packaging against Taiwan Semiconductor Manufacturing Company (TSMC) and Advanced Semiconductor Engineering (ASE) is a multi-year, capital-intensive bet with no guaranteed customers yet.

The distinction that mattered for TOTO applies here: value accrues not to companies that mention AI in their strategy, but to those sitting where demand compounds, capacity stays tight, and substitution is difficult.

For the display sector, that points toward the equipment and component suppliers feeding the transition — and, eventually, toward whichever panel makers successfully cross into packaging.

Where Traders Can Position

China’s domestic policy adds a tailwind for BOE specifically. Beijing continues channelling funding into hard-tech industries, and BOE’s AI push aligns directly with those national priorities. (For context on China’s policy-driven tech funding direction, see: China’s IPO Revival: Innovation-Driven but Politically Curated)

Looking broader at access, the tradeable exposure sits in the supply chain.

- AMAT sits at the intersection of display panel fabrication and semiconductor advanced packaging. Every AI-enhanced line flows through its equipment.

- TSMC and UMC handle increasingly complex display controllers for AI-enabled panels.

- NVDA provides compute infrastructure for AI factories and digital twin workflows.

- LPL offers direct exposure to OLED and AI-integrated features but carries margin risk as AI manufacturing becomes standard.

- AAPL and HPQ benefit indirectly from improved panel quality and efficiency.

China’s domestic policy adds a tailwind for BOE specifically. Beijing continues channelling funding into hard-tech industries, and BOE’s AI push aligns directly with those national priorities. (For context on China’s policy-driven tech funding direction, see: China’s IPO Revival: Innovation-Driven but Politically Curated)

What Still Needs Proving

The optimistic view: display technology is being reinvented, with legacy infrastructure and process knowledge finding new purpose as AI demand outpaces traditional semiconductor supply.

The cautious view: this could be a survival strategy dressed in AI language. Turning glass interposer reviews into revenue is a multi-year, billion-dollar challenge.

Signals to watch:

- AMAT and ASML guidance: If quarterly reports call out display-related AI investment separately from general semiconductor capex, it becomes a tradeable catalyst rather than just a conference talking point.

- Concrete packaging commitments: Any display maker announcing packaging capacity with customer contracts before late 2027 (industry timeline for first commercial glass-based applications) carries outsized market signal value.

The pattern is consistent: when AI demand outstrips existing capacity, the market starts looking at who else has the physical infrastructure and process expertise to fill the gap. Display makers, it turns out, have both.

Whether they can convert that into earnings is the trade.

Interested in tracking price movements in the display technology sector? Download the VT Markets app to monitor real-time CFD price action related stocks.

Tap for Quick Refresher!

How is AI transforming the display manufacturing industry?

AI is powering intelligent factory floors, improving production efficiency, enabling advanced semiconductor packaging, and even repurposing display factories into data centers.

Why are display makers entering semiconductor packaging?

A supply gap in 2.5D and 3D packaging, driven by AI chip demand, is attracting display makers. Their expertise in glass substrates and precision lithography overlaps with packaging requirements.

Which companies are key players in this AI + display ecosystem?

Applied Materials (AMAT), ASML, Lumentum (LITE) in production; TSMC, UMC in chips; Nvidia (NVDA) in AI compute; LG Display (LPL), Apple (AAPL), and HP (HPQ) in end devices.

What timelines are relevant for commercial packaging adoption?

First commercial applications of glass-based advanced packaging are expected around late 2027, making it a medium-term market opportunity for display makers.

How does China’s policy affect BOE and the AI display push?

Beijing’s funding for hard-tech industries provides tailwinds for BOE’s AI initiatives, aligning the company’s strategy with national innovation priorities.

Start trading now – Click here to create your real VT Markets account